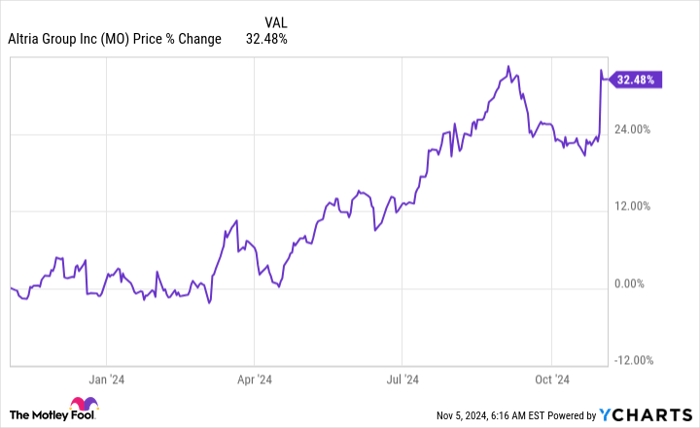

Shares of Altria (NYSE: MO) have had an awesome run over the previous 12 months, gaining greater than 30% in worth. Third-quarter 2024 earnings received buyers notably excited, with the inventory rallying sharply after the discharge. However is Altria’s enterprise actually that good? To reply that query that you must dig into the numbers a bit of bit. However you solely should scratch the floor earlier than you understand that the long-term image is probably not pretty much as good as administration needs you to imagine.

What does Altria do?

It is very important step again and perceive the core enterprise wherein Altria operates. Via the primary 9 months of 2024, the corporate generated roughly $18 billion in income. Of that complete, smokable products introduced in $15.9 billion in income, or about 88% of the whole. Smokable merchandise embrace each cigarettes and cigars, with cigarettes accounting for about 98% of quantity. Inside cigarettes, the Marlboro model accounted for simply over 90% of quantity. All this leads very clearly to the truth that Altria is a high-end branded cigarette firm.

Picture supply: Getty Photos.

However proper now, Altria is spending a variety of time highlighting the NJOY vaping enterprise it just lately acquired. It’s the first “division” that’s mentioned in any element within the firm’s third-quarter 2024 earnings launch. It is smart that Altria would spotlight the positives. And there are main positives with NJOY, however you must take them with a grain of salt.

For instance, within the third quarter, NJOY’s consumables cargo quantity rose 15.6% in comparison with the identical quarter a 12 months in the past. NJOY gadgets shipments rose greater than 100%! And NJOY gained 2.8 share factors 12 months over 12 months in its product class. That is all excellent information, however NJOY is working off of a small base. A swift enchancment in efficiency is to be anticipated simply from plugging NJOY into Altria’s distribution system alone. Put one other approach, the product’s progress is sweet information, however given the state of affairs it is not stunning information in any approach.

Altria’s issues have not gone away

That is the place buyers must be extra discerning. The corporate is cheerleading its greatest attributes because it makes an attempt to downplay its worst ones. And whereas NJOY is a vibrant spot, it’s so small that the earnings it generates is assessed within the “different” class. The “different” class on the income statement, for reference, accounted for a lot lower than 1% of income within the third quarter regardless of all of that progress at NJOY administration informed buyers about. It is not even a rounding error.

In reality, all of that progress at NJOY seemingly did not assist Altria’s prime line in any respect by the primary 9 months of the 12 months, since general income declined 2.5% 12 months over 12 months in that span. The reason being actually easy to grasp, too, if you take a look at the place most of Altria’s income is generated. That is nonetheless a premium cigarette firm. Interval. Laborious cease. NJOY is a superb story, nevertheless it simply is not significant at this level, and it’ll probably be a very long time earlier than it’s significant sufficient to offset the continuing declines within the firm’s cigarette enterprise.

To place a quantity on the declines, Marlboro quantity was down 7.5% within the third quarter and was off by 9.4% by the primary 9 months of 2024. Altria’s non-Marlboro manufacturers carried out even worse. However this is the large takeaway — even common worth will increase weren’t sufficient to offset the hit from quantity declines by the primary 9 months of 2024.

This isn’t a dividend inventory for the faint of coronary heart

The issue from an investor’s viewpoint is that Altria pays an enormous 7.5% dividend yield, which is sort of a siren name to dividend investors. It will possibly help that yield for now regardless of the continuing declines in its most essential enterprise. However long-term dividend buyers must ask how lengthy this will final provided that the substitute product Wall Road is so enthusiastic about continues to be only a tiny a part of Altria’s enterprise.

If you happen to do resolve to purchase Altria, be sure to comply with the inventory like a hawk. Most buyers, nevertheless, will in all probability be higher off trying elsewhere for dependable passive earnings.

Do you have to make investments $1,000 in Altria Group proper now?

Before you purchase inventory in Altria Group, think about this:

The Motley Idiot Inventory Advisor analyst crew simply recognized what they imagine are the 10 best stocks for buyers to purchase now… and Altria Group wasn’t certainly one of them. The ten shares that made the minimize might produce monster returns within the coming years.

Think about when Nvidia made this listing on April 15, 2005… for those who invested $1,000 on the time of our advice, you’d have $904,692!*

Inventory Advisor supplies buyers with an easy-to-follow blueprint for fulfillment, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of November 4, 2024

Reuben Gregg Brewer has no place in any of the shares talked about. The Motley Idiot has no place in any of the shares talked about. The Motley Idiot has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.

{kind=link}