Superior Micro Units AMD shares misplaced 17.1% previously month underperforming the Zacks Laptop & Know-how sector’s return of 0.9%.

AMD shares have additionally lagged chip friends – NVIDIA NVDA and Intel – previously month. Shares of NVIDIA and Intel returned 9.5% and 4.2%, respectively, in the identical timeframe.

AMD shares have been affected by a sluggish fourth-quarter 2024 view.

Discover the most recent EPS estimates and surprises on Zacks Earnings Calendar.

The corporate expects fourth-quarter 2024 revenues of $7.5 billion (+/-$300 million). On the mid-point of the income vary, this represents year-over-year development of roughly 22% and sequential development of roughly 10%.

Sequentially, AMD expects robust development within the Knowledge Heart, Shopper and Gaming segments. 12 months over 12 months, the corporate expects Knowledge Heart and Shopper phase revenues to extend considerably, pushed by its robust product portfolio. The Embedded and the Gaming phase revenues are anticipated to say no.

One Month Efficiency

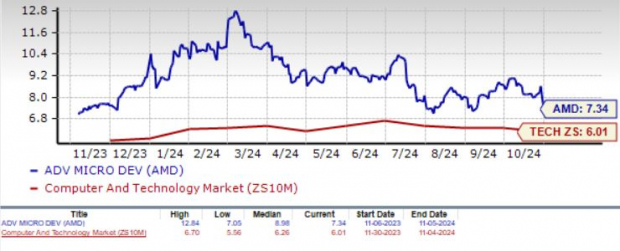

Picture Supply: Zacks Funding Analysis

AMD’s Estimate Revision Exhibits Downward Development

The Zacks Consensus Estimate for AMD’s fourth-quarter 2024 earnings is presently pegged at $1.06 per share, down 2.8% over the previous 30 days. The determine suggests 37.66% year-over-year development.

The consensus mark for fourth-quarter 2024 revenues is pegged at $7.51 billion, indicating 21.82% development 12 months over 12 months.

Superior Micro Units, Inc. Worth and Consensus

Advanced Micro Devices, Inc. price-consensus-chart | Superior Micro Units, Inc. Quote

The Zacks Consensus Estimate for AMD’s 2024 earnings is presently pegged at $3.30 per share, down 1.8% over the previous 30 days. The determine suggests 24.53% development from the determine reported in 2023.

The consensus mark for 2024 revenues is pegged at $25.66 billion, indicating 13.16% development from the determine reported in 2023.

Robust Semiconductor Demand to Help AMD’s Prospects

AMD has been benefiting from robust gross sales of its knowledge middle chips that help hyperscalers and energy AI and Generative AI (Gen AI) functions. Robust demand for these chips drove international semiconductor gross sales within the third quarter of 2024. The Semiconductor Business Affiliation reported 23.2% year-over-year development in international semiconductor gross sales, which hit $166 billion.

Exiting third-quarter 2024, AMD’s public cloud cases elevated 20% 12 months over 12 months to greater than 950, with Microsoft MSFT, AWS, Uber, and Netflix deploying it at scale.

Meta Platforms META alone employed greater than 1.5 million EPYC CPUs globally to energy its social media platforms. EPYC occasion adoption by enterprise clients additionally expanded, with notable wins from Adobe, Boeing, and Tata, amongst others.

The World Semiconductor Commerce Statistics (“WSTS”) initiatives international gross sales to succeed in $611.2 billion, indicating a 16% improve from 2023. This means an uptick from the earlier steering of 13.1%. This bodes properly for AMD.

IDC’s expectations for 2024 semiconductor gross sales are extra optimistic. It expects greater than 20% year-over-year development, primarily fueled by heightened demand for AI chips and restoration in smartphone demand. For 2025, WSTS expects international gross sales to develop 12.5%, finally reaching $687.4 billion.

Wealthy Associate Base, Acquisitions Help AMD’s Prospects

Enterprise and Cloud AI buyer pipeline stays sturdy. AMD and its companions, together with Microsoft, Oracle, DELL, HPE, Lenovo, and Supermicro, have intuition platforms in manufacturing.

AMD’s acquisitiveness primarily goals to cut back the technological hole with NVIDIA within the ongoing race for AI dominance. It has been on an acquisition spree to strengthen its AI ecosystem.

The corporate just lately closed the acquisition of Helsinki, Finland-based Silo AI. AMD is strengthening its knowledge middle AI footprint with the introduced acquisition of ZT Programs for roughly $4.9 billion in money and inventory.

AMD’s initiatives to develop its portfolio are making it well-positioned to problem NVDA not solely within the knowledge middle market but additionally within the rising AI-enabled client PC market.

Within the third quarter of 2024, AMD expanded its footprint amongst power, know-how, and automotive corporations, together with Airbus, FedEx, HSBC, Walgreens and others.

New choices just like the Intuition MI325X accelerator are serving to to develop AMD’s footprint within the knowledge middle market. AMD has launched the Ryzen AI 300 Collection, the third technology of AMD AI-enabled cell processors, and Ryzen 9000 Collection processors for laptop computer and desktop PCs.

AMD Shares – Is it the Proper Time to Purchase?

AMD’s increasing portfolio, because of acquisitions of Silo AI and ZT Programs, is predicted to spice up its top-line development. Buyers who already personal the inventory could anticipate the corporate’s development prospects to be rewarding over the long run.

Nonetheless, AMD’s near-term prospects are boring, given the weak point within the Embedded phase amid stiff competitors from NVIDIA. AMD has a Development Rating of D, which makes the inventory unattractive for growth-oriented traders.

AMD inventory can also be overvalued, because the Worth Model Rating of D suggests a stretched valuation at this second.

The inventory is buying and selling at a premium with a ahead 12-month Worth/Gross sales of seven.34X in contrast with the Zacks Laptop and Know-how sector’s 6.01X.

Worth/Gross sales Ratio (F12M)

Picture Supply: Zacks Funding Analysis

AMD presently has a Zacks Rank #3 (Maintain), suggesting that it might be sensible to attend for a extra favorable entry level to build up the inventory. You may see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks Names #1 Semiconductor Inventory

It is only one/9,000th the dimensions of NVIDIA which skyrocketed greater than +800% since we really useful it. NVIDIA remains to be robust, however our new prime chip inventory has way more room to growth.

With robust earnings development and an increasing buyer base, it is positioned to feed the rampant demand for Synthetic Intelligence, Machine Studying, and Web of Issues. World semiconductor manufacturing is projected to blow up from $452 billion in 2021 to $803 billion by 2028.

See This Stock Now for Free >>

Advanced Micro Devices, Inc. (AMD) : Free Stock Analysis Report

Microsoft Corporation (MSFT) : Free Stock Analysis Report

NVIDIA Corporation (NVDA) : Free Stock Analysis Report

Meta Platforms, Inc. (META) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.

{kind=link}