For the majority of retired Americans, Social Security isn’t simply some check that is available in the mail or is transferred right into their bank account when month-to-month. Instead, it’s an important income source that assists senior citizens make ends fulfill. The program is in charge of drawing almost 22.5 million individuals out of destitution yearly, 16.1 countless which are grownups aged 65 as well as over. Additionally, given that 2002, a minimum of 80% of evaluated retired people have actually informed nationwide pollster Gallup that their Social Safety and security advantage is a “significant” or “small” income source.

Due to the vital duty Social Safety and security plays in the monetary wellness of senior citizens throughout retired life, there’s perhaps no occasion a lot more awaited than the program’s yearly cost-of-living change (SODA POP) news throughout the 2nd week of October.

Picture resource: Getty Images.

Below’s exactly how your Social Safety and security “increase” is computed

Social Safety and security’s soda pop is the “raising” the program passes along to recipients most years to make up inflation— the increasing rate of products as well as solutions. Keep in mind: “Elevate” remains in quote marks to stand for that this is a rise in advantages made to match the price of rising cost of living as well as not to exceed it, which can occur with an extra conventional raising from a company.

Before 1975, Social Safety and security’s soda pop was appointed randomly by unique sessions of Congress. The good news is, the program has actually had an extra regular inflationary secure ever since with the Customer Cost Index for Urban Breadwinner as well as Clerical Employees (CPI-W). The CPI-W has a handful of major spending categories as well as a shopping list of subcategories, each with its very own particular portion weighting. These weightings are what permit the CPI-W to be trimmed to a solitary number, which can after that be quickly contrasted to the previous month or year to establish whether rising cost of living or depreciation (dropping costs) is happening.

Although the United State Bureau of Labor Stats reports the CPI-W monthly, only readings from the third quarter (July via September) element right into Social Safety and security’s soda pop estimation. While the various other months can assist recognize patterns with rates, they have no influence on the “raising” Social Safety and security’s greater than 66 million recipients would certainly obtain in 2024.

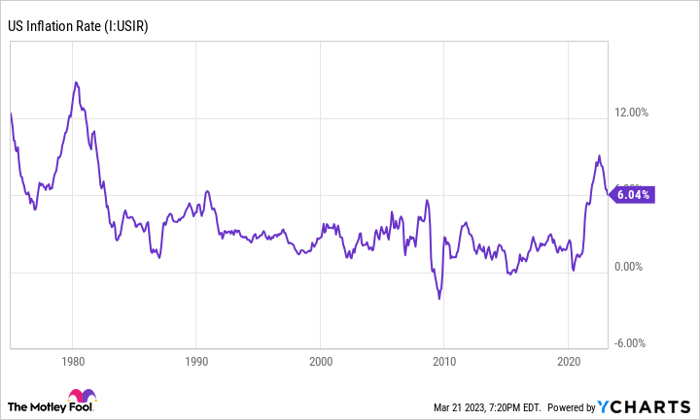

U.S. Inflation Rate information by YCharts.

A very early keep reading Social Safety and security’s 2024 soda pop isn’t motivating

For the program’s almost 49 million retired employees, Social Safety and security’s soda pop for the existing year was traditionally high. The 8.7% “increase” they obtained stands for the biggest year-over-year portion rise in advantages in 41 years as well as is the biggest nominal-dollar boost given that the program was authorized right into legislation.

Regrettably, Social Safety and security’s 2024 soda pop does not appear it’ll be a repeat of 2023– and even close, for that issue.

According to a really early prognostication sent out in an e-mail to CBS MoneyWatch from Mary Johnson, an elderly Social Safety and security plan expert at The Elderly People Organization (TSCL), “[T] he [2024] soda pop appear like it will certainly be listed below 3% as well as can fall under the 2% and even reduced variety by the 3rd quarter if that 12-month standard [for the CPI-W] remains to decrease.”

Whereas the typical retired person appreciated a passionate $146 rise to their month-to-month Social Safety and security sign in 2023, an approximately 2% to 3% soda pop would certainly correspond to an extra moderate $37 to $55 increase per sign in 2024.

In Between June 2022 as well as February 2023, the trailing-12-month price of rising cost of living, as gauged by the Customer Cost Index for All Urban Customers (CPI-U), has declined from a peak of 9.1% to 6% as well as is anticipated to proceed dropping. The Federal Get boosting rate of interest at the fastest rate in greater than 4 years, together with oil costs backing well off their 2022 highs, is the excellent tornado for a substantial decrease in the united state rising cost of living price, in addition to a much lower Social Security COLA next year.

Picture resource: Getty Images.

A possibly frustrating 2024 “increase” is just half the problem for retired people

Nonetheless, a significantly reduced “increase” in 2024, contrasted to this year, is just component of the trouble for senior citizens that depend on their Social Safety and security checks to cover their costs. The even more encompassing problem is that the CPI-W doesn’t do a particularly good job of measuring inflation for the mass of the program’s receivers.

At its core, the CPI-W tracks the investing behaviors of “city breadwinner as well as clerical employees,” as its complete name states. The important things is, city breadwinner as well as clerical employees are commonly working-age Americans that aren’t obtaining a Social Safety and security advantage. Because the majority of Social Safety and security recipients are senior citizens, the CPI-W tends to undernourished costs that make up a bigger portion of their investing, such as treatment as well as sanctuary, while overweighting expenses that aren’t as vital, like education and learning, clothing, as well as transport.

Based upon a record launched by TSCL in 2015, the buying power of a Social Safety and security buck hasdeclined by an almost unfathomable 40% since 2000 What $100 in Social Safety and security earnings can acquire in 2000 can currently just acquire $60 well worth of those very same products as well as solutions.

Maybe one of the most irritating element of the CPI-W’s imperfections is that legislators from both events know they exist, as well as they concur something must be done. Nonetheless, Democrats as well as Republicans are approaching a fix from opposite ends of the spectrum as well as consequently have not had the ability to locate any kind of commonalities. Given that bipartisan participation is called for to get to the 60 ballots required to change Social Safety and security in the Us senate, it’s not likely we’ll see this Social Safety and security shortage dealt with anytime quickly.

The $21,756 Social Safety and security bonus offer most retired people entirely ignore

If you resemble the majority of Americans, you’re a couple of years (or even more) behind on your retired life cost savings. Yet a handful of obscure “Social Safety and security tricks” can assist make certain an increase in your retired life earnings. For instance: one very easy technique can pay you as high as $21,756 even more … yearly! When you find out exactly how to optimize your Social Safety and security advantages, we believe you can retire with confidence with the assurance we’re all after. Simply click here to discover how to learn more about these strategies.

The has a disclosure policy.

The sights as well as viewpoints revealed here are the sights as well as viewpoints of the writer as well as do not always mirror those of Nasdaq, Inc.

{kind=link}