In a shocking flip of occasions, a decide dominated in favor of the U.S. authorities and blocked the proposed merger between purse and style rivals Capri Holdings (NYSE: CPRI) and Tapestry (NYSE: TPR). The Federal Commerce Fee (FTC) sued to dam the merger in April after Tapestry agreed to purchase Capri final 12 months, arguing that the mixture would damage shoppers and depart much less inexpensive purse choices.

The FTC lawsuit was broadly considered as a protracted shot, as there was little priority to dam offers within the style business and it could be tough to show {that a} deal would damage shoppers or enhance costs.

Each Capri’s Michael Kors model and Tapestry’s Coach model, in the meantime, are sometimes considered as accessible luxurious manufacturers. On its web site, Coach has purses priced as excessive as $10,000, whereas Kors has baggage priced as excessive as $3,300, so they don’t seem to be promoting low-cost merchandise.

The information despatched Capri’s inventory crashing, as its shares fell greater than 45% whereas Tapestry shares climbed double-digits. Now that the merger is presently blocked, what ought to traders do with the shares?

Capri

Capri, which is residence to luxurious manufacturers Versace and Jimmy Choo, along with Kors, has been struggling for the reason that announcement of the merger. As such, the plunge in its shares ought to maybe not come as an entire shock.

The corporate has seen its income decline for seven straight quarters, together with a 13% decline final quarter, which led to June. Kors is its largest model and noticed gross sales sink 14%, with over 20% declines in Europe and Asia. Working revenue for the model, in the meantime, plunged 42%.

Issues weren’t any higher for Versace, which noticed its gross sales drop by 15%. Europe was its weakest area, with gross sales down 22%, whereas gross sales within the Americas had been down 15%. Asia solely noticed a 3% decline in gross sales.

Jimmy Choo, identified for girls’s footwear, was Capri’s best-performing model, however gross sales had been down 5.5%. The corporate noticed constructive gross sales within the U.S., however Asia was a weak spot, with income down 17%.

Capri was in limbo for a 12 months whereas it was ready for its acquisition to undergo, so it is probably not shocking that its efficiency has been subpar. Usually, administration will not make any large strategic shifts forward of being acquired, whereas the uncertainty can influence firm morale and trigger a expertise drain.

From a valuation standpoint, the crash in shares lowers Capri’s forward price-to-earnings ratio (P/E) a number of to 9. Nonetheless, that is a bit greater than the place the inventory traded earlier than the acquisition announcement.

CPRI PE Ratio (Forward) information by YCharts.

In the meantime, traders are left with an organization that is been rudderless for the previous 12 months and now should embark on a turnaround. Whereas the corporate ought to see renewed focus, the injury has been accomplished and a turnaround is probably not simple. Even with the massive drop, I would steer clear of the inventory.

Picture supply: Getty Pictures

Tapestry

The federal government’s blocking of the take care of Capri might be the very best factor for Tapestry. The corporate should pay Capri as much as $50 million if the deal is rejected, however that is a small value to pay.

In the meantime, Tapestry, which owns Coach, Kate Spade, and Stuart Weitzman, has been performing significantly better than Capri. Whereas its gross sales fell 2% final quarter, they had been flattish on a constant-currency foundation. In the meantime, its adjusted earnings per share (EPS) fell from $0.95 to $0.92.

Along with being Tapestry’s largest model, Coach has been its best-performing, with gross sales up 2% on a constant-currency foundation in fiscal This fall and 4% for the 12 months. Kate Spade and Stuart Weitzman, in the meantime, each noticed gross sales fall final quarter and for your entire 12 months.

General, Tapestry has seen strong development in Europe, which appears to have been Capri’s weakest market, whereas North American gross sales had been down barely. Asia (exterior of China) has seen strong development, though Chinese language gross sales final quarter had been down 10%.

The corporate is anticipating modest development in fiscal 2025 with some slight margin enchancment. It had beforehand mentioned that if the Capri acquisition did not undergo, it could use its robust free money stream for capital-allocation functions, notably to purchase again shares.

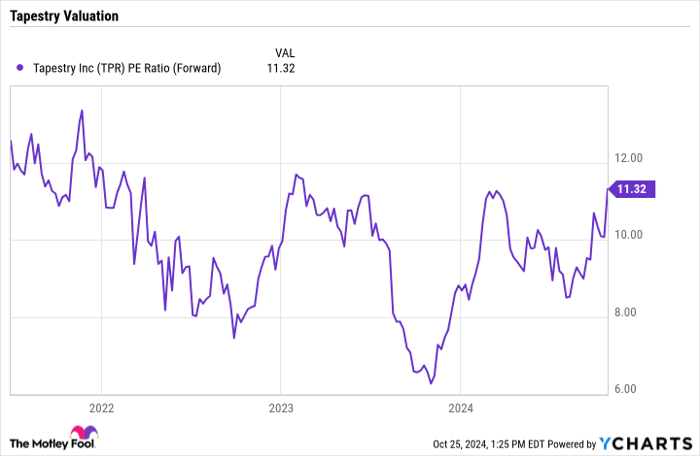

Buying and selling at a ahead P/E of 11, Tapestry is near buying and selling on the ranges earlier than the merger announcement.

TPR PE Ratio (Forward) information by YCharts.

Whereas the corporate has clearly carried out higher than Capri, it hasn’t precisely been a robust grower, as gross sales have not modified a lot throughout the previous two fiscal years. The corporate now should search for one other method to reinvigorate development. Given its lack of development and bounce in inventory value, the inventory presently seems to be fairly pretty valued.

Do you have to make investments $1,000 in Capri proper now?

Before you purchase inventory in Capri, think about this:

The Motley Idiot Inventory Advisor analyst workforce simply recognized what they imagine are the 10 best stocks for traders to purchase now… and Capri wasn’t one in every of them. The ten shares that made the reduce might produce monster returns within the coming years.

Contemplate when Nvidia made this record on April 15, 2005… in case you invested $1,000 on the time of our suggestion, you’d have $861,121!*

Inventory Advisor gives traders with an easy-to-follow blueprint for fulfillment, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of October 28, 2024

Geoffrey Seiler has no place in any of the shares talked about. The Motley Idiot recommends Tapestry. The Motley Idiot has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.

{kind=link}