Chipotle Mexican Grill (NYSE: CMG) has been within the headlines of late for the unsuitable causes. The most important attention-grabber was the departure of the corporate’s well-respected CEO. However a fast 20% value decline is one other worrying bit of knowledge that is exhausting to disregard. If you’re a long-term development investor, nonetheless, listed here are three causes to stay optimistic about Chipotle inventory.

1. The drop in Chipotle’s shares is not uncommon

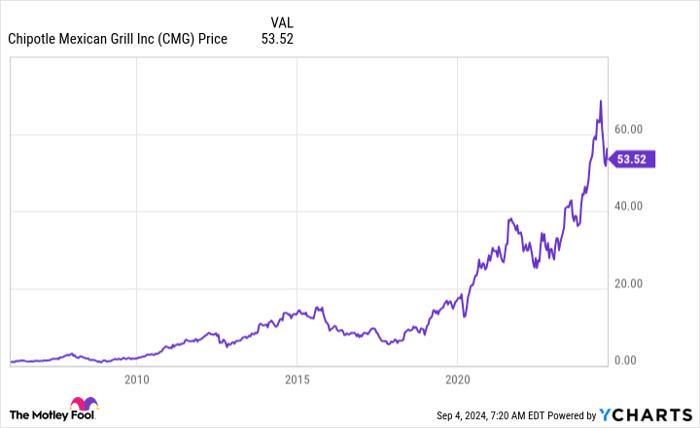

Growth stocks have a behavior of lurching larger, pulling again to consolidate these positive aspects, after which lurching larger once more. It may be exhausting to stay round by the ups and downs, however for firms which have an extended runway for development forward, it’s usually the very best plan of action. With that background, Chipotle’s present value retreat is not actually odd for the corporate.

Actually, because the graph above highlights, that is the seventh pullback of 20% or extra. Sometimes the inventory has declined even additional, reaching 50% a couple of occasions and even 75% as soon as. And but the present pullback has left the inventory 20% or so under its all-time excessive, which additionally occurs to be the 52-week excessive. So this has been a gradual climb larger with fast downdrafts alongside the best way. Or, in plain English, that is simply how the inventory strikes.

Chipotle operates round 3,500 eating places. Taco Bell, owned by Yum! Manufacturers, has round 8,500 places. That means that long-term, Chipotle might nonetheless double in dimension and never totally saturate its meals area of interest.

2. Chipotle is working from a place of energy

Having loads of room for extra shops is one factor, however the extra essential a part of the story is that Chipotle is not doing badly proper now. Actually, it’s doing extraordinarily effectively. Within the second quarter of 2024, same-store sales soared 11.1%. That is an enormous quantity within the meals sector, the place low-single-digit same-store gross sales development is taken into account good. General gross sales, helped by new retailer openings, elevated 18.2% to $3 billion. Once more, that is a reasonably strong quantity for a restaurant.

To be honest, Chipotle most likely cannot proceed to place up numbers like this without end. So affordable buyers ought to anticipate some pullback in efficiency. Nonetheless, it could be exhausting to counsel that Chipotle’s enterprise is doing badly immediately. It’s, the truth is, executing on the prime of its recreation despite the fact that the inventory value would counsel the alternative.

3. Chipotle’s CEO is forsaking a company

That brings the story to the most important destructive headline of the 12 months, Chipotle’s CEO abruptly leaping ship to Starbucks (NASDAQ: SBUX). Brian Niccol was effectively revered within the restaurant area and was credited with serving to to place Chipotle on a extra stable upward trajectory. So maybe his departure is a destructive.

But although he headed up a big enterprise, he wasn’t the one particular person working it. He leaves a crew of hand-selected leaders behind him and a enterprise that’s working effectively. The brand new CEO may have huge sneakers to fill, however this is not a turnaround scenario or an organization that wants a giant refresh. The interim CEO, Scott Boatwright, was the corporate’s chief working officer, so he is aware of the corporate effectively. And a high-level worker who not too long ago introduced his retirement has agreed to stay round a bit to assist out. All in, Chipotle looks like it’s nonetheless in good arms.

Must you regulate the corporate due to the CEO’s departure? Sure! Must you fret that the top is nigh? Completely not.

Chipotle’s bumpy experience larger

Growth stocks usually traverse a bumpy street that leads steadily larger over time. That is the story behind Chipotle to this point, and there is no specific motive to consider its present stock-price pullback shall be any completely different from earlier pullbacks. The corporate is performing effectively and its operations are sound. Panicking simply does not appear warranted by the info proper now.

Must you make investments $1,000 in Chipotle Mexican Grill proper now?

Before you purchase inventory in Chipotle Mexican Grill, take into account this:

The Motley Idiot Inventory Advisor analyst crew simply recognized what they consider are the 10 best stocks for buyers to purchase now… and Chipotle Mexican Grill wasn’t one in all them. The ten shares that made the minimize might produce monster returns within the coming years.

Take into account when Nvidia made this record on April 15, 2005… should you invested $1,000 on the time of our suggestion, you’d have $630,099!*

Inventory Advisor supplies buyers with an easy-to-follow blueprint for fulfillment, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of September 3, 2024

Reuben Gregg Brewer has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Chipotle Mexican Grill and Starbucks. The Motley Idiot recommends the next choices: brief September 2024 $52 places on Chipotle Mexican Grill. The Motley Idiot has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.

{kind=link}