Fifteen months in the past, we contrarians started the bond bandwagon. It is exhausting to imagine now, however again then the monetary fits hated mounted revenue. We light their fears, purchased bonds and benefited.

Now, nevertheless, I am cautious on bonds. The ten-year Treasury yield has been on a tear since Jay Powell first lower the Fed Funds Fee.

Bond Vigilantes Scoff at Powell’s Fee Cuts

You possibly can’t make these things up. On September 18, Powell lower charges by 50 foundation factors. Nonetheless, this was solely the “quick finish” of the yield curve. The ten-year yield in the meantime (the “lengthy finish”) popped from 3.7% to almost 4.5% in a matter of weeks!

Oh, the irony! The bond vigilantes put Powell on discover that inflation is not lifeless but. So, did Powell take the trace? Nope–he lower charges once more.

If it appears like Powell is sort of a determined poker participant on tilt, effectively, it will get worse. The Fed Chair is conscious, as we all are, that Trump dislikes him. Powell has already mentioned he’ll not resign if requested by the President-elect.

Which is a humorous query as a result of Powell doesn’t report back to the President. Even perhaps funnier that he answered it.

Web-net we must always search for Powell to maintain his punch bowl flowing to ease the political strain on him. He is already been conducting quiet QE. Why not maintain loosening cash?

Liquidity is bullish for shares, which will increase customers’ spending energy and the costs of what they purchase. In the meantime, we’ve got three pillars of Trump 2.0: financial development, tariffs and decrease immigration. Three extra boosts for larger costs.

Which suggests bonds, particularly the vanilla type issued by the US Treasury, should not probably the most interesting place to stash cash for 10 years. Would you wish to lend to Uncle Sam for a decade at simply 4%+ yearly given this backdrop?

Bonds change into scorching potatoes on this setting. These fixed-rate payers lose luster as charges rise.

Floating-rate bonds (with coupons that enhance alongside rates of interest) haven’t got this drawback. They maintain their worth and might even respect.

Tickers? Let’s begin with these three ETFs, which mix for greater than $11 billion in belongings beneath administration:

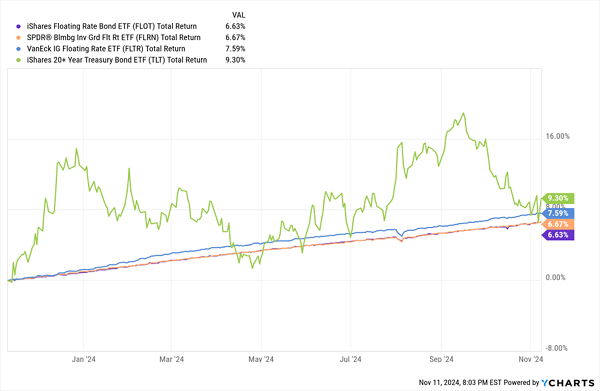

- iShares Floating Fee Bond ETF (FLOT, 5.5% SEC yield): FLOT, the most important pure-play floating-rate bond ETF, tracks an index of roughly 375 investment-grade floating-rate bonds. The portfolio is roughly three-quarters invested in corporates, together with a heavy 50% weighting in banking-sector bonds. Nonetheless, the remaining quarter is in supranational bonds–debt issued by worldwide organizations such because the Worldwide Financial Fund and the World Financial institution.

- SPDR(R) Bloomberg Funding Grade Floating Fee ETF (FLRN, 5.4% SEC yield): FLRN prices the identical (0.15% in annual bills) as FLOT and even tracks the identical index, but it surely’s not an identical. There are just a few small variations, together with a barely larger weighting in finance-sector bonds and just a little extra publicity to AAA-rated debt.

- VanEck IG Floating Fee ETF (FLTR, 5.6% SEC yield): FLTR really supplies just a little differentiation. This can be a international floating-rate portfolio–55% is invested in U.S. bonds, with the remaining 45% unfold throughout seven different developed nations, together with Australia, Canada, and the UK. Additionally, this fund is solely made up of company bonds, 85% of that are from the monetary sector.

All three of those funds are solely (or just about solely) invested in bonds with maturities of 5 years or much less. That is par for the course for floating-rate funds.

Common bonds inside this maturity schedule have additionally suffered because the Powell fee lower, simply not by as a lot as longer-dated bonds. So floating-rate bond ETFs, shorter-term as they is likely to be, are nonetheless very a lot bucking the pattern:

However Wow, They Do not Actually Transfer All That A lot, Do They?

Sure, these floating-rate ETFs are about as regular as regular will get, they usually’ve actually made it by the previous few months with gusto.

However as loopy because it sounds, they depart loads of yield on the desk.

Floating-rate closed-end funds (CEFs) can get us into the double digits–though we do want to find out whether or not we’re shopping for excessive yields, or high-yield traps.

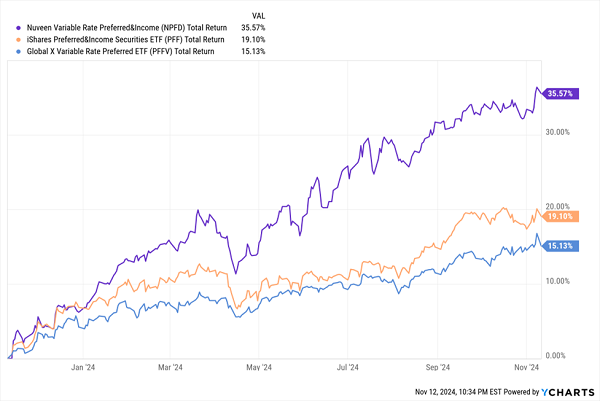

Nuveen Variable Fee Most well-liked & Earnings Fund (NPFD, 10.5% distribution fee) is an fascinating different to bond-specific floating-rate mounted revenue.

This comparatively younger fund, which got here into being rather less than three years in the past, primarily invests in corporations’ variable-rate preferred securities (and different variable-rate income-producing securities). And like most most popular funds, it is heavy in financials. Actually, its 4 prime industries–diversified banks (32%) akin to JPMorgan Chase (JPM) and Citigroup (C), insurance coverage (16%), capital markets (12%), and regional banks (11%)–are all throughout the sector. Credit score high quality is sort of excessive, too; greater than 75% of belongings are invested in investment-grade preferreds.

I first wrote about this fund a couple of years ago in the midst of a stoop for preferreds and famous that it was bleeding much more profusely than its plain-vanilla counterparts throughout each conventional and variable-rate points.

However that CEF juice (learn: 37% debt leverage) is working in NPFD’s favor on this a part of the speed cycle, and it has managed to maintain pushing larger following the September fee lower.

Administration Is Merely Higher Armed and Positioned to Seize Upside

NPFD additionally offers us the month-to-month dividends we worth, and it has even put collectively a pleasant little streak of distribution hikes.

Valuation is just a little tough to get a learn on, nevertheless. This Nuveen CEF trades at a 6% low cost to web asset worth (NAV), which is not unhealthy, however there’s restricted historical past; its 1-year common low cost is deeper, although, at 11%.

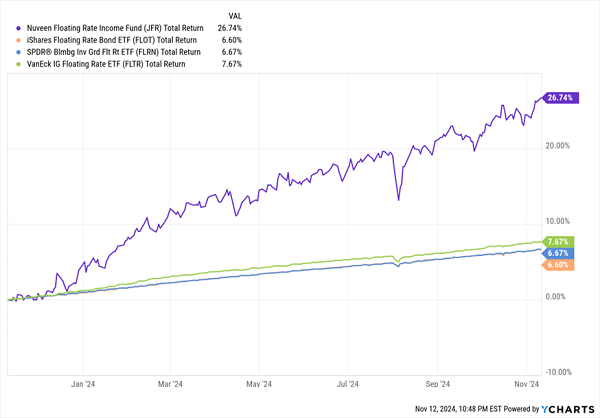

One other Nuveen fund price a glance is the Nuveen Floating Fee Earnings Fund (JFR, 11.4%), which is a extra conventional variable-rate CEF with an enormous month-to-month payout.

That is an actively managed portfolio of roughly 430 company floating-rate bonds. Credit score is on the junkier aspect, with solely 10% of belongings in investment-grade bonds. However it’s properly unfold out–five sectors have double-digit weightings, led by client discretionary at 19% and knowledge know-how at 17%.

Maybe most useful for the time being, although, is its holdings’ maturities. JFR’s bonds aren’t notably lengthy, however they’re longer than the ETFs above, with 58% within the 0- to 4-year vary, and the remaining in 5- to 9-year territory.

That, and a heaping serving to of debt leverage (38%), have helped JFR rocket previous its extra tempered ETF rivals:

However persistence is a advantage right here. The cat is essentially out of the bag, with NPFD’s low cost to NAV closing from its roughly 9% five-year common to a at present slim 3%.

The One 11% Dividend to Personal Now

That 11% dividend is likely to be out of bounds for now, however my One 11% Dividend to Own Now continues to be firmly in “purchase” territory.

Safe dividends are the final word security net–they’re money in your pocket, proper right here, and proper now, regardless of whether or not your tickers are flashing inexperienced or purple.

The dividend shares above present loads of market cowl even at single-digit yields.

So simply think about what sort of safety towards volatility you possibly can get from a 11% dividend.

My One 11% Dividend to Own Now is a uncommon machine able to producing a merely ludicrous amount of money. A 11% yield, in probably the most sensible phrases, is:

- $916 a month from a mere $100,000 funding

- $55,000 a year–a correct wage in lots of elements of the U.S.–from a mere $500,000 nest egg

- A wild $110,000 yearly in case you have one million bucks to place to work

Paid out for sitting round and doing nothing however ready.

That form of cash does not simply purchase you issues.

It buys you consolation. It buys you peace of thoughts. It buys you a daily good night time’s sleep–where you cease questioning and worrying about which means the market’s winds will blow subsequent.

It might even purchase you the flexibility to dwell off of dividends alone, with out ever laying a finger in your nest egg.

However you do not have a lot time. In case you miss the deadline to get on the listing now, in just a few days, you possibly can be leaving cash on the table–and won’t be capable of lock on this 11% when the subsequent distribution comes round.

Additionally see:

Warren Buffett Dividend Stocks

Dividend Growth Stocks: 25 Aristocrats

Future Dividend Aristocrats: Close Contenders

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially replicate these of Nasdaq, Inc.

{kind=link}