Newmark Group, Inc. NMRK has seen its inventory decline 10.1% over the previous month, closing at $12.58 on Thursday. This efficiency lags behind each the Zacks Real Estate – Operations business in addition to the S&P 500 composite.

Macroeconomic uncertainty, tariff woes and expectations of a chronic high-interest price setting have been affecting the general market in latest occasions. Business actual property transactions, too, stay shrouded with elevated rates of interest and financial uncertainty. Traders have thus adopted a cautious strategy, delaying the closing timeline for transactions.

The present panorama has not spared NMRK both and has led to the inventory’s latest underperformance. Regardless of the challenges within the industrial actual property sector, the corporate’s efficiency lately displays its strategic strengths.

Nevertheless, earlier than rapidly deciding to take away this inventory out of your portfolio or speeding to purchase after the dip, it’s essential to judge whether or not NMRK has sturdy progress potential and assess whether or not the present issues might considerably impression its efficiency.

One-Month NMRK Inventory Value Efficiency

Picture Supply: Zacks Funding Analysis

What Can Drive Newmark Inventory Up?

Sturdy Capital Markets Efficiency and Market Share Positive factors: Newmark is having fun with sturdy capital markets efficiency and market share good points. Capital markets’ revenues in fourth-quarter 2024 elevated by 20.0%, extending a streak of 5 consecutive quarters of double-digit progress. Excluding the fourth quarter-2023 Signature transactions, Newmark surpassed business efficiency, reaching a roughly 113% improve in whole Capital Markets notional volumes final quarter. This progress encompassed a 209% rise in Mortgage Brokerage and Debt Placement, an 85% improve in GSE/FHA origination, and a 71% enhance in Funding Gross sales. Pushed by its energy in information facilities amid the rising demand from hyperscale AI customers, the corporate achieved a report $9.2 billion in industrial volumes throughout Leasing and Capital Markets.

Newmark has a confirmed report of gaining share in U.S. capital markets. Between 2015 and 2024, its share of U.S. funding gross sales elevated from 3.3% to eight.7% of whole business volumes. Over the identical interval, its whole debt market share grew from 1.5% to eight.9% of whole U.S. business originations.

With $2.1 trillion in U.S. industrial and multifamily mortgage maturities anticipated by 2027, 25% being probably troubled in response to Newmark Analysis, the corporate is well-positioned to learn from elevated transaction exercise. Aside from driving its capital markets enterprise, this quantity of maturities can be anticipated to drive demand for Newmark’s different companies, together with leasing, property administration, valuation & advisory, and servicing.

Resilient Administration and Servicing Income Development: Newmark’s administration companies and servicing enterprise present a secure base for revenues and earnings. The corporate has achieved stable progress in administration and servicing revenues and goals to develop whole revenues for these service traces to greater than $2 billion inside 5 years. From 2017 to 2024, charges from these companies surged by 219%, whereas whole revenues grew by 190%, establishing these as Newmark’s fastest-growing service traces since its IPO.

Sturdy Monetary Place and Money Circulate Era: Newmark enjoys a robust monetary place and is well-poised for progress with stable money move technology capabilities. Its capital-light enterprise mannequin (it doesn’t personal actual property), low leverage (internet leverage ratio of 1.1 as of Dec. 31, 2024) and stable curiosity protection ratio (7.9) allow continued funding in progress initiatives whereas sustaining monetary stability. It additionally enjoys sturdy money move, producing $437.6 million in working money move in 2024.

With no near-term debt maturities, leverage nicely beneath its long-term goal of ≤1.5X, and two-thirds of bills being variable, Newmark is well-positioned to navigate potential market disruptions.

Worldwide Growth Presents Lengthy-Time period Development Potential: Newmark’s latest growth in Europe — with the launch of capital markets and leasing operations in Germany within the fourth quarter of 2024 and the addition of prime expertise in France, the U.Ok., and different international markets — positions the corporate to capitalize on progress alternatives.

Newmark’s non-U.S. revenues have grown from 0.9% of whole revenues in 2017 to 13.3% in 2024, reflecting round 59% income CAGR. Furthermore, with solely 13.3% of revenues coming from worldwide markets for Newmark, in comparison with 28-46% for its full-service U.S.-listed public friends, this actual property operations firm has ample room for additional progress.

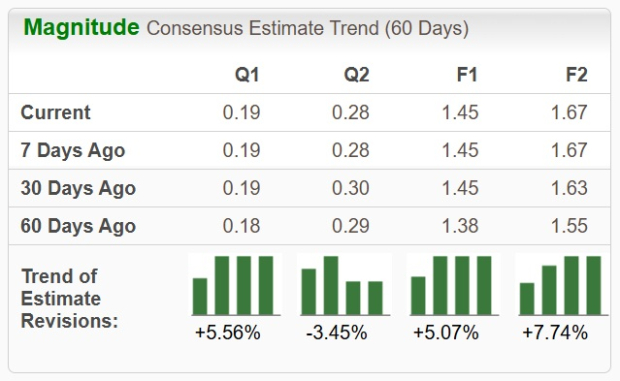

Estimate Revision Favoring the Inventory

Equally, analysts appear to be bullish about Newmark Group’s prospects, as indicated by the Zacks Consensus Estimate for EPS’s upward revision for each 2025 and 2026 over the previous two months. These estimates point out year-over-year progress charges of 17.9% and 14.8% for 2025 and 2026, respectively.

Picture Supply: Zacks Funding Analysis

Discover the newest EPS estimates and surprises on Zacks Earnings Calendar.

From a valuation perspective, Newmark Group shares current a lovely alternative. NMRK is taken into account undervalued, implying that the market is but to totally acknowledge or worth the corporate’s potential progress prospects or earnings potential.

Presently, NMRK is buying and selling at a ahead 12-month price-to-earnings of 8.40X, which is at a reduction to the business common of 15.47X and decrease than its one-year median of 9.62X. Value-to-earnings is a generally used a number of for valuing actual property operations shares. The inventory can be buying and selling at a reduction to its business peer CBRE Group, Inc.’s CBRE present ahead 12-month P/E of 20.75X and Jones Lang LaSalle Integrated’s JLL P/E of 14.61X.

Ahead 12 Month Value-to-Earnings (P/E) Ratio

Picture Supply: Zacks Funding Analysis

Last Ideas on NMRK

Newmark Group has demonstrated sturdy operational momentum, pushed by market share growth, strategic investments, and a resilient enterprise mannequin. Regardless of macroeconomic uncertainties, Newmark’s sturdy capital markets platform, servicing enterprise and powerful money technology place it nicely for future progress.

Related constructive sentiments of analysts are additionally echoed within the upward estimate revision developments, and the valuation additionally seems to be low cost. All these point out that assuming an growing place on this Zacks Rank #1 (Sturdy Purchase) inventory shall be a prudent choice earlier than the value strikes considerably away from its present degree. You possibly can see the complete list of today’s Zacks #1 Rank stocks here.

Solely $1 to See All Zacks’ Buys and Sells

We’re not kidding.

A number of years in the past, we shocked our members by providing them 30-day entry to all our picks for the whole sum of solely $1. No obligation to spend one other cent.

1000’s have taken benefit of this chance. 1000’s didn’t – they thought there should be a catch. Sure, we do have a purpose. We wish you to get acquainted with our portfolio companies like Shock Dealer, Shares Beneath $10, Know-how Innovators,and extra, that closed 256 positions with double- and triple-digit good points in 2024 alone.

Newmark Group, Inc. (NMRK) : Free Stock Analysis Report

Jones Lang LaSalle Incorporated (JLL) : Free Stock Analysis Report

CBRE Group, Inc. (CBRE) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.

{kind=link}