When you have been taking a break from your loved ones on Christmas Day, you might have caught my article on how Jay Powell’s latest “hawkish reduce” is about to gentle a fireplace below high-yielding (and tax-free!) municipal bonds.

Here is why: Jay reduce charges by 1 / 4 level in December, however gave buyers a stern pre-holiday “talking-to,” with the Fed slashing its rate-cut forecast to 2 from 4 in 2025.

Shares, as you’d anticipate, threw a one-day match. However this is the factor: The yield on the 10-year Treasury be aware (the so-called “lengthy finish” of the yield curve, which has a thoughts of its personal) spiked.

In different phrases, the Fed reduce however rates of interest nonetheless rose.

The bond market is clearly telling Jay, in no unsure phrases, that the job on inflation is not achieved. And eventually, he seems to be listening. Which is the place our contrarian alternative in muni bonds is available in.

“Grownup within the Room” Jay Set to Set off the Subsequent Muni-Bond Rise

You and I each know that everybody is anticipating inflation (and subsequently rates of interest) to go increased below Trump 2.0. And within the longer run, that could be true. However, contrarians we’re, we additionally know that when everybody expects one thing to occur, one thing else often does.

What we’re speaking about right here will be the first funding shock of 2025: That charges prime out and switch decrease due to Jay’s new-found sternness. As they do, bond costs will rise.

Charges down, bonds up. That is simply the best way it goes in bond-land.

And at this time’s excessive 10-year yield means bonds are despised proper now. Did somebody say “despised”? We’re ! Particularly after we can faucet these “loathed” earnings performs for a number of the most secure, highest (to not point out tax-advantaged) dividends on the board: these paid out by municipal bonds.

Muni-Bond CEFs: Our Supply of Regular 7.8% Dividends (and 0% Taxes)

“Munis” are issued by state and native governments, primarily to fund infrastructure initiatives. The important thing factor we love about them is that, for many People, muni dividends are tax-free. That may quantity to quite a bit–especially for these within the prime tax bracket.

As you possibly can see under, to get the equal of a 7.8% tax-free muni-bond dividend–the payout on the closed-end fund (CEF) we’ll delve into next–a top-bracket taxpayer would want a 12.9% yield on a taxable payout, like that on a inventory.

Supply: Bankrate.com

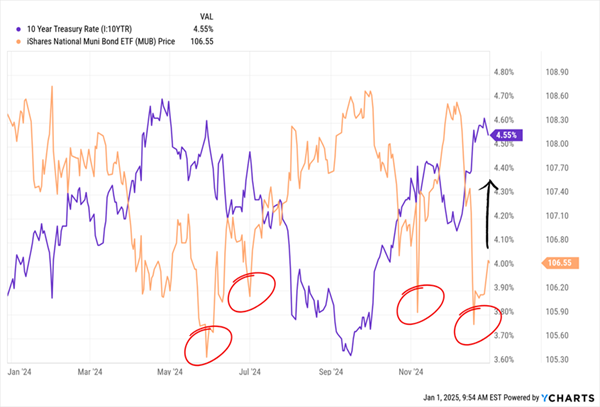

Upside? Nicely, the connection between munis and the 10-year Treasury charge is evident within the chart under. When you’d purchased the muni-bond benchmark ETF, the iShares Nationwide Muni Bond ETF (MUB) every time charges peaked, you’d have grabbed your self some good upside.

Shopping for Munis on The Dip At all times Pays (and Our Subsequent Purchase Window Is Right here)

However we’re not shopping for MUB, for a pair causes:

- Wimpy payouts: MUB yields simply 3% as I write this.

- No reductions: Since ETFs (not like CEFs) can problem new shares at will, they at all times commerce at (or near) their portfolio values. As I write this, MUB trades at a 0.15% low cost to internet asset worth (NAV)–basically zero!

As an alternative, we’re shopping for probably the most discounted muni-bond CEF held by my Contrarian Income Report service, the Nuveen High quality Municipal Earnings Fund (NAD).

As talked about, this one kicks out a 7.8% tax-advantaged yield, and that payout comes our means month-to-month. That drives the 12.9% taxable-equivalent yield we noticed above, for my top-bracket ballers.

However the low cost is the straw that actually stirs the drink right here. As I write this, NAD trades at an unwarranted 8.3% low cost to NAV. That is properly under its pre-election peak of 5.5%. And think about that again on the finish of 2021, earlier than the Fed’s final rate-hike cycle began, NAD was near par.

Each of these numbers counsel that at this time’s low cost, with charges taking a look at a good bit of upside resistance from right here, is overdone.

And on the subject of previous efficiency, NAD is a lock, helped by the workforce at Nuveen. They handle $429 billion price of bonds. When municipalities problem bonds–or suppose about it–they name the massive whale Nuveen. The muni big throws its purse round to safe the very best offers for its buyers.

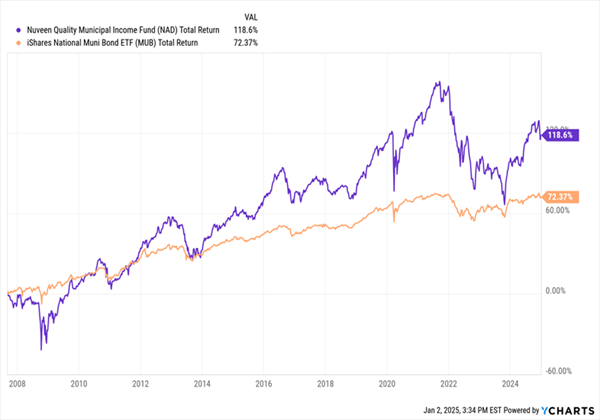

That is helped NAD (in purple under) outrun MUB during the last 17 years or so, since MUB’s launch:

NAD Delivers a Double (All in Dividend Money)

Certain, NAD’s return was extra risky than that of the ETF, however do not forget that reinvested dividends drove this achieve, so NAD buyers have been getting extra liquidity than MUB holders, who needed to rely extra on worth good points because of the fund’s lame dividend.

This additionally reveals how essential it’s to carry these funds for the lengthy haul to reap the most important tax-advantaged returns from them. And naturally, these tax benefits are sweeter whenever you apply them to a 7.8% present yield than they’re on a 3% payer!

In terms of munis (or any bonds, actually), we have to take note of two key dangers: length danger and credit score danger.

Credit score danger is a non-issue with NAD, thanks primarily to munis’ security, with default charges within the basement, under 0.1% since 2013. With 1,171 bonds in its quiver, even within the unlikely case that one did default, the affect on the portfolio can be microscopic.

Period danger? That, in a nutshell, is the priority that increased charges sooner or later will make the yields on the fund’s present holdings look lame. But when charges prime out and transfer decrease, long-duration bonds rule, and NAD solely has about 13% of its holdings maturing within the subsequent 13 years. Its common length, adjusted for leverage, is a prolonged 12.5 years.

Talking of leverage, the fund borrows towards 40% or so of its portfolio, which magnifies its returns in an up market and, sure, can enlarge losses when markets drop (which is why NAD’s efficiency is extra risky than that of MUB within the final chart we checked out).

Right here, we belief Workforce Nuveen to deftly throttle leverage as situations change. Decrease charges would imply NAD’s present leverage would give its worth an additional raise. And, in fact, the fund’s borrowing prices would dip, too, additional supporting our excessive (and tax-free) payouts.

This Pressing 2025 Purchase (11% Yield!) Is Set to Drop Its Subsequent BIG Payout

NAD, with its large tax-free dividend, is a nice purchase for 2025. With a payout like that (and confirmed long-term efficiency), it is a lifeline for the 12 months forward, which I anticipate to be extra risky than 2023 or 2024.

That is our theme for 2025: Large, secure dividends that enable us to maintain our payments paid (and our retirement totally funded) it doesn’t matter what occurs with the Fed or the markets.

Purchase NAD Now–However Do not Overlook to Seize This 11% Payer, Too

Which brings me to the different huge payer I am pounding the desk on now. Not solely does this 11% payer have a protracted historical past of retaining its large payout rolling shareholders’ way–it sports activities a historical past of dividend progress, too.

This unique decide is the final word funding for 2025, and I do not need you to be left with out entry to its large, regular money stream. And with its subsequent huge payout set to drop quickly, the time to get in is now.

Whenever you look again on this purchase in early 2026, I feel you will be thrilled on the double-digit earnings stream you have collected. However that will not occur should you do not make your transfer straight away. Click here to learn more about this incredible 11% payer and get in line for its next regular payout.

Additionally see:

Warren Buffett Dividend Stocks

Dividend Growth Stocks: 25 Aristocrats

Future Dividend Aristocrats: Close Contenders

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.

{kind=link}