- Stocks rebound as bond yields fall back, but US inflation report poses a risk

- Yen firmer after Ueda confirmed as nominee for BoJ governor

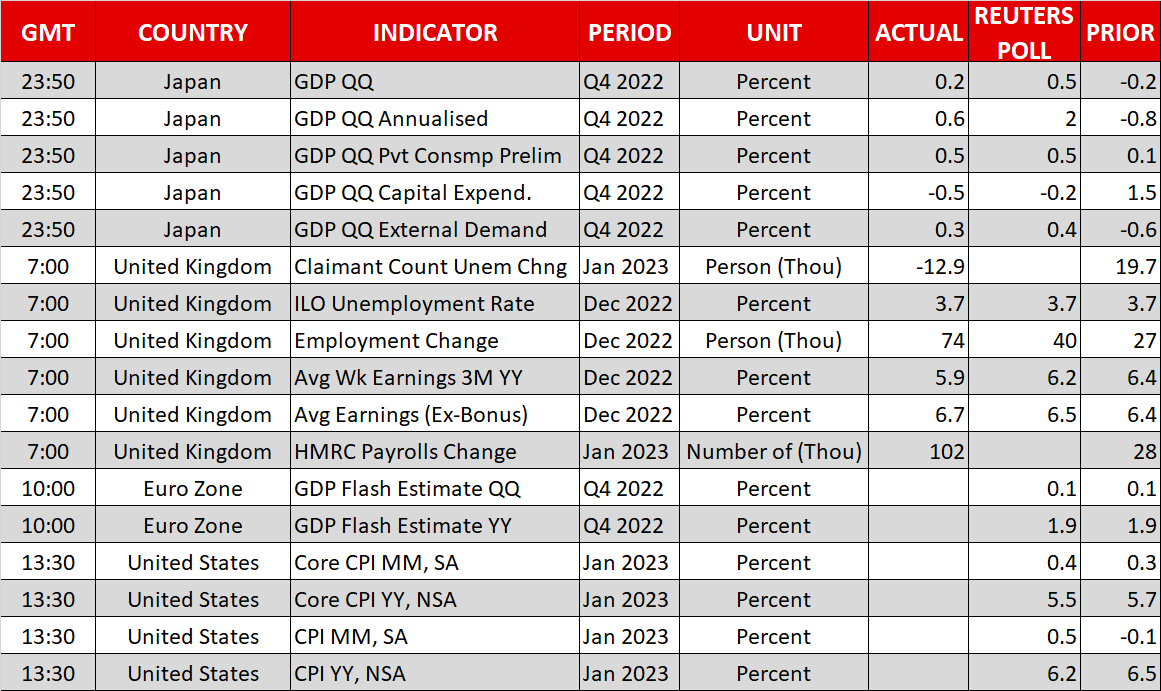

- Pound inches higher on UK jobs data, gold finds support ahead of US CPI

Equity markets fearless ahead of CPI test

It’s all about the US inflation report today as the January figures (due at 13:30 GMT) will either endorse the view that disinflation is taking hold or point to a long battle ahead to contain price pressures. After the recent remarks on disinflation from Fed Chair Powell and the run of softer-than-expected CPI releases, it’s easy for the markets to pin their hopes on the former.

But there’s a danger that the January prints will go the opposite way. Business surveys for last month painted a mixed picture for input costs while the U.S. Bureau of Labor Statistics made upward revisions to the December numbers. Moreover, the January report will be the first to use a different methodology for calculating the consumer price index, hence, the risk that the forecasts end up being way off the mark is quite high.

Analysts are predicting that the headline CPI rate will continue its downward decline to fall from 6.5% to 6.2% y/y, while core CPI is expected at 5.5% y/y.

Despite some jitters last week, equity markets seem confident about the forecasts, staging a rebound on Monday. All three of Wall Street’s indices rallied more than 1%. E-mini futures are slightly in the red today, but European shares are extending their gains.

Lower yields fuel risk-on sentiment

The surge in Treasury yields took a breather on Monday and the 10-year yield is slipping further today. This could just be a combination of caution in the run up to the CPI report and a technical correction. But investors may also be reacting to the New York Fed’s latest consumer expectations survey that showed income expectations dropping at the sharpest pace on record in January, in a sign that consumers are reining in their expectations for pay increases.

Either way, tech stocks were buoyed, with reports that Facebook (NASDAQ:) parent Meta is considering further job cuts adding more fuel to the bounce back, which spread across the other tech heavy weights such as Apple (NASDAQ:) and Microsoft (NASDAQ:).

However, there’s a danger that markets are setting themselves up for a fall as an upside surprise in today’s inflation numbers is bound to spark a significant selloff. Perhaps the biggest risk is not so much the data itself but the fact that several Fed policymakers are due to speak a few hours later at separate events.

Yen climbs as BoJ nomination puts spotlight on yield cap

The 10-year Japanese government bond (JGB) yield bucked the trend on Tuesday to press higher, albeit to be capped by the Bank of Japan’s upper yield target of 0.50%. The yield target is under renewed pressure following the Japanese government’s decision to appoint Kazuo Ueda as the Bank of Japan’s next chief.

Even though there’s little to suggest that Ueda would be in favour of a rapid rise in interest rates, it’s very likely that the yield curve control policy’s days are numbered and investors are anticipating some kind of a policy overhaul soon after he takes over from Kuroda.

The speculation of such a shift has helped the yen recover from multi-decade lows versus the US dollar, although its gains today are very modest, with weaker-than-expected Q4 GDP figures possibly weighing on the currency.

Pound gets jobs boost, CPI next

The pound was also firmer on Tuesday as its one-week-old rebound was bolstered by strong jobs data. Employment in the UK grew by more than expected in the three months to December, while wage growth excluding bonuses accelerated to 6.7%. If tomorrow’s CPI numbers are equally strong, it could make it more difficult for the Bank of England to think about pausing its rate hikes soon.

The New Zealand dollar is the only major that’s down against the greenback after two-year inflation expectations fell in the RBNZ’s latest quarterly survey.

Gold reverses higher after hitting one-month low

In commodities, gold is attempting to recover from one-month lows, edging up to around $1,860/oz. The precious metal has not benefited much from the recent headlines of surveillance balloons, suspected to be from China, flying over US airspace. On the other hand, reports that US Secretary of State Antony Blinken could hold talks with Chinese officials at the Munich Security Conference later this week suggest the situation is unlikely to escalate.

Nevertheless, gold prices are probably taking their cues from the moves in yields and the dollar in heading higher today.

{kind=link}