There is a very particular sort of magic that occurs once you’re doing all your taxes and the quantity in crimson immediately flips to inexperienced.

You realize the one I imply. One second, the display is telling you that you simply owe the IRS $500. The subsequent? You are watching a refund. An actual, precise refund. One thing we hadn’t seen in our family in years.

My husband and I simply sat there blinking.“Did that basically simply occur?”

It did. And the rationale was my residence workplace.

To be clear, this wasn’t some sketchy tax trick or loophole I noticed on TikTok. This was areputable deduction obtainable to self-employed of us who usually and completely use a part of their residence for enterprise. I might began doing extra freelance modifying and writing over the previous couple of years and had arrange an LLC each for legal responsibility causes and, frankly, as a private finance experiment.

I figured I might be capable of write off apparent enterprise bills — issues like the pc software program I used, my laptop computer, possibly even a brand new desk chair. However what I did not notice is that I may additionally deduct a proportion of my utilities. My web invoice. My pest management. Even the price of the housekeeper who cleans that room.

All of it.

And it added as much as over a thousand {dollars} in tax financial savings.

That is the story of how my residence workplace — the identical one I take advantage of to file invoices, write articles, and host Zoom calls with no fewer than three espresso mugs on my desk — ended up being one in every of my favourite tax wins of the yr.

And since I genuinely such as you — you take the time to learn my article, after all I such as you — and need you to get each greenback you are entitled to, I will allow you to in on what I’ve realized. I had no concept how useful this deduction might be till I dug into the main points myself. So if it might probably aid you too? Even higher!

The IRS Has Guidelines — This is Easy methods to Make Certain You Qualify

I need to be actually clear about this upfront as a result of the IRS could be very particular about what qualifies — and what would not.

To take the house workplace deduction, you must meet two major necessities:

Unique Use: The house have to be used completely for enterprise. Which means no dual-purpose rooms. In case your visitor room additionally doubles as your Zoom background, sorry — that is not going to chop it. It needs to be an area that is put asideparticularly for work.

Common Use: You additionally want to make use of the house usually for your corporation. Not simply as soon as a month when inspiration strikes or when the lounge is just too loud. It must be yourconstant work location.

The house would not have to be an entire separate room, however it does have to be a clearly outlined space that meets each of these circumstances. So sure, if you happen to’ve carved out a devoted desk nook the place you run your aspect enterprise — and you utilize it completely and usually — it would qualify.

Additionally essential: This deduction is barely obtainable to self-employed people. When you’re a W-2 worker working from residence, even full-time, this does not apply to you. (Sorry — I do not make the principles. However possibly it is price citing with Congress.)

Once I first began my LLC, I did not know most of this. I might heard the phrase “residence workplace deduction” thrown round earlier than, however I assumed it was just for individuals who ran full-blown companies out of their homes — not somebody like me who sometimes labored from the kitchen desk, the sofa, or wherever the toddler chaos wasn’t.

It wasn’t till I sat all the way down to do our 2023 taxes — the primary yr my LLC was absolutely up and working — that I began trying into what really went into the varied self-employment deductions. I realized concerning the common and unique use necessities, and it clicked. “Oh, this deduction is not only for individuals with fancy residence studios… It is for anybody working a legit enterprise who’s prepared to carve out the house.”

So I made some modifications. We had a spare downstairs room that wasn’t getting used for a lot — a form of unintended sitting room that nobody ever sat in. It was quiet, had a door, and simply so occurred to be the right measurement. So I claimed it. I moved in my desk, arrange store, and made it my devoted workplace house.

By the point we hit 2024, I had a completely certified residence workplace — and an entire new appreciation for a way productive (and tax-efficient) a single room might be.

How I Turned a Random Room right into a Legit Tax Deduction

My residence workplace is roughly 280 sq. toes, which shakes out to simply over 9% of our whole residence. Which means I get to deduct 9% of eligible family bills — issues like our electrical energy, web, and owners insurance coverage — as a result of these issues assist my work and my workspace.

Now, the IRS provides you two methods to calculate your deduction:

– The Simplified Technique, which is simply $5 per sq. foot (as much as 300 sq. toes). So, for my 280 sq. foot workplace, I may’ve simply claimed a flat $1,400 and referred to as it a day.

– The Common Technique, which is what I selected. This methodology takes a bit extra work (you fill out Kind 8829), however it lets me deduct a proportion of precise bills for issues like utilities, insurance coverage, repairs, pest management, housekeeping — and even depreciation on the home.

That half is wild. We usually take the standard deduction on our taxes, which implies we do not get to itemize issues like mortgage curiosity or actual property taxes.

However with the house workplace deduction, we get to carve out simply the portion of these bills that applies to my workspace. So though we’re not itemizing on our major return, we nonetheless get to deduct a portion of our mortgage curiosity and property taxes — only for the house workplace.

I believe I needed to learn that half 3 times earlier than it clicked. However yep — it is allowed.

Electrical energy? Web? Pest Management? Sure, You Can Most likely Deduct That

Earlier than we go any additional, let me simply say this loud and clear: I’m not an accountant.

When you’re fascinated about taking the house workplace deduction, please discuss to a professional tax skilled. This text is simply me, a finance nerd, sharing my very own expertise and what I realized alongside the best way.

Okay? Okay. Let’s get into the great things.

When you use the common methodology for the house workplace deduction — which is what I did — you basically get to separate sure residence bills between private and enterprise use, based mostly on how a lot of your house you utilize for work.

For me, that is about 9% of our residence. My workplace is 280 sq. toes, and that is sufficient to qualify for a reasonably significant slice of bills I used to be already paying.

This is the way it breaks down:

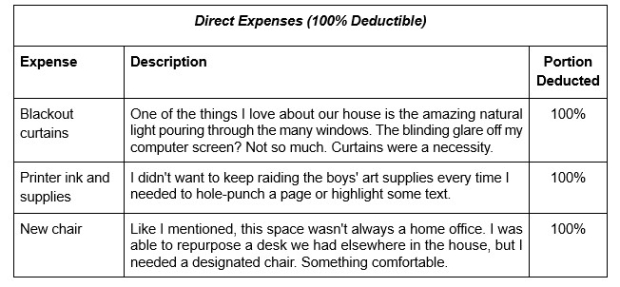

Totally Deductible “Direct” Bills

These are prices that apply solely to your workplace. For instance, I put in blackout curtains in my workplace to assist with Zoom lighting. As a result of these curtains solely profit the workplace, that is thought of a direct expense — and that value is 100% deductible.

Identical goes for issues like:

– Workplace-specific repairs (e.g., fixing the door, changing carpet)

– Portray the partitions in your workplace

– A separate business-only cellphone line

Partially Deductible “Oblique” Bills

These are prices that apply to the complete home, however since your corporation is benefiting from a portion of them, you possibly can deduct a proportion. In my case, meaning 9% of:

– Mortgage curiosity

– Actual property taxes

– Electrical energy and gasoline

– Web

– House owner’s insurance coverage

– Pest management

– Cleansing providers

All of these turned oblique residence workplace bills. And that is the place issues get fascinating.

As a result of we usually take the usual deduction, we do not itemize our mortgage curiosity or property taxes. However once you use the common methodology to your residence workplace, you do get to deduct the business-use portion of these prices, even if you happen to’re taking the usual deduction on the remainder of your return.

Which means I bought to jot down off a chunk of my mortgage curiosity and property taxes that will in any other case simply be… nothing. They do not depend towards our customary deduction, and so they do not assist us in some other means. However due to the house workplace deduction, they did assist — and lowered our taxable earnings within the course of.

(And since that is a enterprise deduction, not an itemized one, it additionally helped decrease the quantity of self-employment tax I needed to pay. Bless.)

Peek Inside My Deduction Listing — and What Shocked Me

Once I sat all the way down to calculate every little thing, I used to be shocked by how shortly the deductions added up. A number of proportion factors right here and there would not sound like a lot… till you notice you are making use of that proportion to your greatest recurring payments.

This is a snapshot of what I deducted — utilizing the common methodology, and based mostly on 9% enterprise use of my residence:

Picture Supply: Zacks Funding Analysis

Picture Supply: Zacks Funding Analysis

Direct bills had been rarer for me — however something that applies solely to the workplace is absolutely deductible. And, after all, these are simply the bills that apply to my residence workplace and my work. What I deduct will probably look very completely different than what another person deducts.

One essential distinction: If I had bought a separate enterprise insurance coverage coverage (or rider for my LLC), that would not be a part of the house workplace deduction. It might be a completely deductible enterprise expense elsewhere on my Schedule C. (Once more: accountant. Speak to 1.)

Yet one more element price noting: When you’re solely utilizing your house workplace for a part of the yr — for instance, you began freelancing in July — you may solely be capable of deduct bills for that portion of the yr. The IRS would not allow you to declare a full yr of deductions for a six-month enterprise. So timing issues.

How My Tax Invoice Went From Crimson to Inexperienced in One Click on

Once I hit “enter” on the final batch of bills, I wasn’t anticipating fireworks.

I used to be simply hoping to knock a pair hundred bucks off our whole tax invoice. Possibly ease the sting a bit. What I did not anticipate was to see our total tax state of affairs flip.

One second, we had been watching a $500 fee due. The subsequent, we had been getting a refund.

And to be clear, this wasn’t magic. It was math. Boring, spreadsheet-driven math — the type that takes some time to enter and even longer to double-check. However when it labored… wow, did it work.

That was the second it hit me: This deduction wasn’t nearly saving a couple of bucks on workplace provides. It was about treating my enterprise — and my time — prefer it issues.

I used to be already paying for electrical energy. Already paying for the web. Already paying for pest management and a housekeeper. Nothing about my life modified — besides the truth that now, a few of these unavoidable prices had been working for me.

And as somebody who’s filed taxes as a W-2 worker for many of my life, I can not overstate what a psychological shift this was. For the primary time, I felt like I wasn’t simply on the hook for taxes — I used to be lastly attending to play by a distinct algorithm.

Nonetheless the identical legal guidelines. Nonetheless absolutely above board. However this time, I really bought to make use of them.

Is the House Workplace Deduction Price It? This is the Sincere Reply

Okay, so, here is the half everybody studying really cares about — is claiming the house workplace deduction really well worth the time and hassle?

That is private finance! So clearly, the reply is… it relies upon.

It is not well worth the trouble if…

– You are a W-2 worker working from residence (sadly, staff aren’t eligible for this deduction).

– You sometimes reply emails out of your sofa and name it a day.

– Your “workplace” can be your visitor bed room, your treadmill room, and your canine’s nap zone.

– Actually any state of affairs meaning you do not meet the “unique and common use” necessities the IRS lays out.

However it’s price exploring if…

– You are self-employed, freelance, or run a enterprise from your house — and that enterprise makes sufficient earnings to warrant listening to taxes within the first place.

– You’ve got bought an area in your house that is used just for work and is used that means persistently.

– You are already paying out of pocket for issues like web, insurance coverage, utilities, and extra — and you would like to show a portion of these prices into tax-deductible enterprise bills.

– You are taking the usual deduction in your taxes and desire a method to nonetheless profit out of your mortgage curiosity and property taxes.

If that is you? Then it may be price taking the time to know how this works.

And once more — I am not a CPA. Please don’t take this as skilled tax recommendation. This is only one private finance nerd attempting to share one thing new that unexpectedly saved me $1,000. And even when the house workplace deduction would not apply to you, nonetheless take this as encouragement to ask higher questions, discuss to your accountant, and dig into what the tax code really permits.

As a result of tax deductions aren’t simply strains on a kind. They are a method to lastly let your cash — and your work — pull their monetary weight.

Make the Most of Your Cash with Skilled Insights

Would you want sensible suggestions and instruments that can assist you navigate at this time’s financial system? Zacks’ free Cash Sense publication cuts via the jargon and offers you actionable suggestions that can assist you get monetary savings, slash taxes and construct an enduring legacy.

From must-see funding concepts to sensible budgeting methods, Cash Sense may also help you develop your wealth intelligently. Subscribe at this time and begin attaining your subsequent monetary purpose! It’s completely free to enroll.

Get Money Sense absolutely free >>

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.

{kind=link}