Vladimir Zakharov

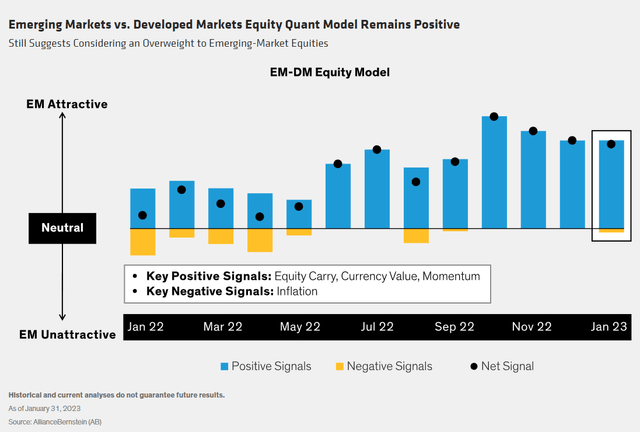

In 2021 and 2022, emerging-market (EM) stocks underperformed developed market equities. Then, last October, our quantitative (quant) signals turned markedly more positive on their relative prospects, based primarily on valuations and currency competitiveness.

These quant signals reinforced our positive fundamental assessment, including early signs of economic reopening in China. Collectively, these lenses made the case that EM looked attractive versus developed markets.

Despite EM’s subsequent outperformance of 12.5% since then (October 31, 2022, through January 31, 2023) our quant scores remain strongly positive for EM stocks (Display), with positive valuation and currency scores now supplemented by positive momentum.

Meanwhile, in fundamental terms, EM’s corporate earnings and economic metrics are holding up better than developed markets; in particular, China’s full-scale reopening and recent adjustments to government policy provide strong support.

While EM continues to face an array of risks from inflation to geopolitics, we think the relative advantage versus developed markets still looks clear.

We still feel that an underweight to risk assets makes sense for muti-asset investors, given that global equities continue to face challenges from slowing growth, elevated inflation and geopolitical risks.

However, we believe tactical positioning and dynamic asset allocation across the widest possible opportunity set can improve risk-adjusted returns. Within equities, our combined multi-asset fundamental and quant analysis suggests that EM still has the brighter outlook relative to developed markets.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

{kind=link}