Actual property funding trusts (REITs) are making a comeback from their post-pandemic downturn–and with the sector nonetheless lagging the inventory market, we have got an opportunity to purchase at engaging reductions.

And we’re effectively arrange so as to add some 7%+ dividend yields–that have began to develop lately–as we do, not in REITs immediately, however in REIT-focused closed-end funds (CEFs).

REITs’ Lag Has Been Dramatic, However the Winds Are Shifting

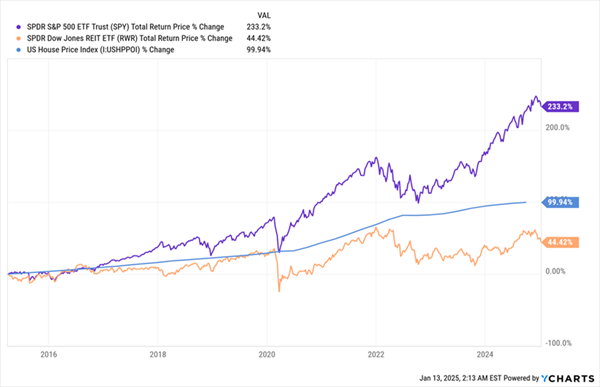

Whereas the S&P 500 has loved a 14.0% annualized return during the last 5 years, as of this writing, REITs, as measured by the efficiency of the benchmark SPDR Dow Jones REIT ETF (RWR), have returned a paltry 2.6% annualized over the identical interval.

That is uncommon, as REITs–landlords who personal properties starting from flats to knowledge facilities and warehouses–usually outperform the S&P 500, as you’ll be able to see by RWR’s long-term return (from the date of RWR’s IPO) beneath.

REITs Sometimes Beat Shares–Till Recently

What makes this development even weirder is that it’s occurring even when there’s not been a shift within the trendlines between REIT costs and home costs. I do know these might sound like separate issues, so let me clarify.

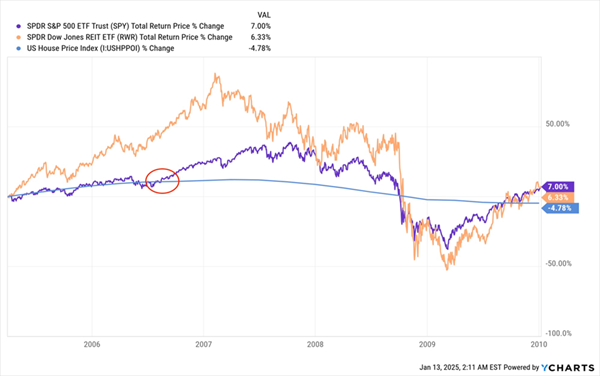

REITs Soar, House Costs Fall

Within the mid-2000s the housing bubble plateaued, as we are able to see within the US Home Value Index (in blue above), however investor fervor for actual property extra usually didn’t, inflicting traders to bid up RWR (in orange) far above the trendline we noticed for homes.

Right now, the development is the precise reverse, with traders bidding much less for REITs (once more in orange) than the development in home costs would recommend is most pure.

Larger Home Costs, Decrease REIT Costs

Housing costs have gained 7.2% per yr on common during the last decade, but RWR has gained simply 3.7% over the identical time interval.

The rationale? A 7.2% annualized acquire is simply an excessive amount of for houses–if we return 33 years, since data of this metric had been first stored, housing rises a mean 4.5% per yr, so we’re due for a pullback. Nonetheless-high 30-year mortgage charges add additional strain right here.

In different phrases, all of the unhealthy information is presently priced into REITs, which as we simply noticed, are lagging house costs.

This actual property pessimism means REITs are presently at a lower cost level than they had been each in 2007, throughout the bubble, and in 2015 to 2019, after the actual property market had recovered and mortgage charges continued to climb.

Actual Property’s Present Sale

That is essential as a result of rates of interest are going to maneuver decrease, both in 2025 or later. And even when they do fall extra slowly than folks first thought, REITs will nonetheless be capable of gather rents from their present portfolios as they look ahead to charges to say no, and nonetheless see their properties’ worth enhance, even when we see no price cuts in 2025. The Fed, nonetheless, has made it clear that it does plan to chop charges.

When charges do fall, mortgages will get cheaper, driving extra actual property demand.

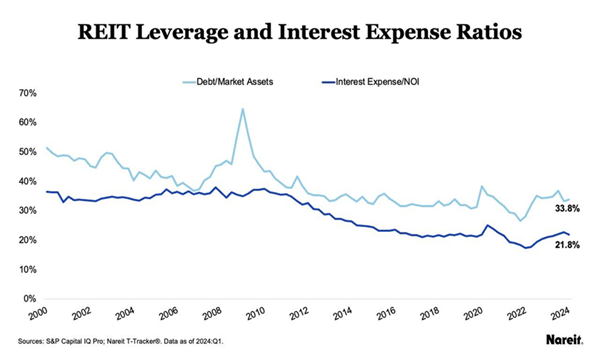

However there’s one other hidden profit for REITs particularly, and that is leverage.

When the Fed lowers rates of interest, it lowers the price of borrowing throughout the market, and meaning REITs can borrow for much less (and naturally, they’ll already borrow for a lot lower than your typical homebuyer). This expands their revenue margins and leads to extra dividend money handed over to traders.

So REITs can benefit from decrease charges to broaden their guide of owned properties.

Will REITs try this? Not solely will they, however the knowledge suggests they’ve already begun.

Earlier than rates of interest first began rising, REITs carried out effectively, because of the bizarre financial components of the pandemic, which meant that leverage was at a multi-decade low in 2021, when rates of interest began to climb.

Whereas REITs have began to borrow once more (see proper aspect of chart above), bringing present leverage ratios to mid-2010s ranges, there’s nonetheless loads of room for them to borrow and broaden.

After they do, this may enhance their web asset values (NAVs) and the entire quantity of earnings they obtain, driving up payouts to shareholders within the type of larger dividends.

We’re already seeing this.

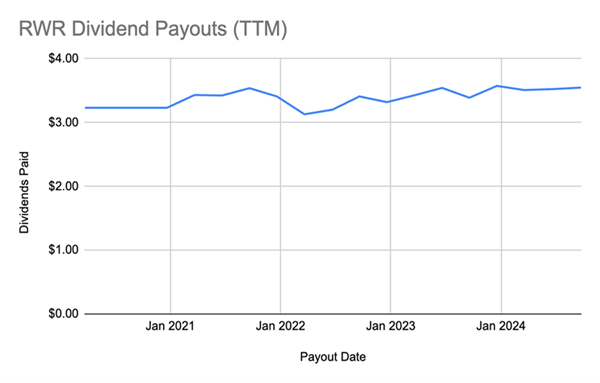

Larger Payouts for REIT Holders

Supply: CEF Insider

After an unsurprising dip in earnings following the pandemic, REITs have been capable of develop payouts so that they are now 7.5% larger than pre-pandemic ranges. But REITs value much less to purchase now than they did again then.

With rates of interest headed decrease (once more, even when slowly) and potential declines in housing costs priced in, REITs are compelling, however there’s one other a part of the story. Some REIT sectors (infrastructure, knowledge facilities and cell towers most notably) are seeing robust progress now, no matter interest-rate tendencies.

Others, like workplace REITs, are recovering from the return-to-office development that’s nonetheless dominating work life, a lot in order that corporations like Starbucks, Amazon and JPMorgan are requiring employees to return to the workplace.

Thus, even when housing costs fall sooner or later, it appears seemingly that different actual property sectors will see costs rise. And even when housing costs do fall, REITs’ potential to borrow at decrease charges will allow them to choose up residential properties and begin renting them out, amassing extra earnings. This implies REITs’ dividend hikes have simply gotten began.

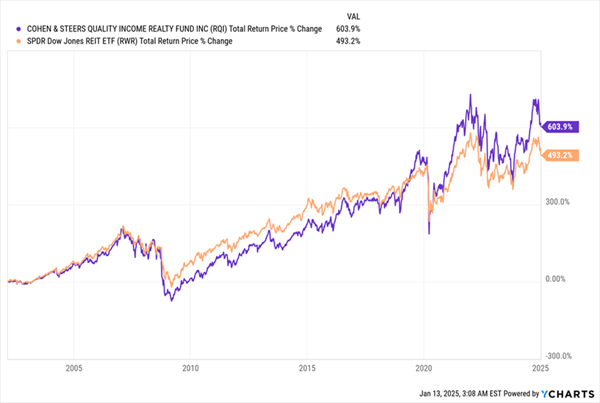

Suppose CEFs, Not ETFs, When Shopping for REITs

RWR’s 3.8% yield is basically too small for us to take critically, so I might recommend taking part in this development by way of a CEF just like the Cohen & Steers High quality Earnings Realty Fund (RQI). The fund’s 8% yield has been consistent–RQI has maintained its dividend for the final 9 years–and its whole returns (in purple beneath) put these of RWR (in orange) to disgrace.

RQI Crushes the REIT Index

Regardless of its outperformance, excessive yield, and constant dividend, RQI trades at a small low cost to NAV–and that low cost is more likely to flip right into a premium if market demand for each excessive yields and actual property continues apace.

Moreover, with 13% of its portfolio in telecommunications, 11.2% in healthcare and 9.4% in knowledge facilities, the fund has positioned itself for these sorts of actual property seeing probably the most demand, whereas its single-family-home portfolio, at 3.5%, is way lighter, that means it is able to revenue from a downturn in house costs in the event that they do occur to take a dip within the brief time period.

Big 9.8% Dividends From … AI?!

REITs are removed from the one investments we are able to faucet by way of high-yielding CEFs. Few folks notice it, however these funds additionally allow us to faucet into AI’s continued progress and get a fats dividend yield in return.

Particular person shares? They simply do not lower it: AI poster boys like NVIDIA (NVDA), Microsoft and the like yield subsequent to nothing.

That is NOT the case with the 4 “AI-Powered” CEFs I am pounding the desk on now. They yield a fats 9.8% on common in the present day and so they’re ALL cheap–so a lot in order that they primarily allow us to purchase the AI shares of their portfolios at costs that have not been accessible to “common” traders for months.

Now could be the time to purchase these 4 spectacular funds and begin reaping massive earnings (and dividends) as AI continues to embed itself in our day-to-day lives.

Additionally see:

Warren Buffett Dividend Stocks

Dividend Growth Stocks: 25 Aristocrats

Future Dividend Aristocrats: Close Contenders

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.

{kind=link}