Sew Repair, Inc.’s SFIX emphasis on enhancing consumer experiences and sustaining a strong monetary basis, together with a debt-free stability sheet, reinforces its potential for sustained profitability. The progressive use of AI and efficient value administration positions the corporate for long-term success. As Sew Repair continues its transformation and descriptions a transparent development technique, it’s well-equipped to navigate the evolving retail panorama.

SFIX has demonstrated spectacular efficiency by rising its RPAC by 4.5% 12 months over 12 months, reaching $533 within the fourth quarter of fiscal 2024. This development displays the corporate’s effectiveness in deepening relationships with core purchasers by means of personalised and versatile procuring experiences.

By rising the variety of objects in a “Repair,” Sew Repair has boosted common order values, resulting in greater consumer spending. This rise in RPAC not solely signifies profitable product optimization but in addition signifies the potential for elevated buyer lifetime worth, which is important for long-term profitability.

Picture Supply: Zacks Funding Analysis

SFIX’s Improvements & Operational Effectivity Bode Nicely

Sew Repair’s proprietary AI expertise performs a pivotal function in delivering personalised consumer experiences at scale, with options like StyleFile contributing to a 5% rise in conversion charges amongst new purchasers. Regardless of income headwinds, the corporate has maintained profitability by means of value management and operational optimization, reaching constructive adjusted EBITDA for seven consecutive quarters.

Within the fourth quarter, the adjusted EBITDA margin rose 90 foundation factors to three%, whereas the gross margin expanded by 50 foundation factors 12 months over 12 months to 44.6%, pushed by higher stock administration and a concentrate on higher-margin private-label merchandise.

The corporate applied a cost-cutting initiative that saved greater than $100 million in promoting, normal and administrative bills in fiscal 2024. Wanting ahead, Sew Repair anticipates extra financial savings in fiscal 2025 to reinforce its backside line. With a transparent three-phase transformation technique — rationalization, constructing and development — the corporate goals to drive income development by fiscal 2026.

Sew Repair concluded the fiscal fourth quarter with $162.9 million in money and no debt, offering the pliability to put money into development initiatives with out monetary burdens. This strong monetary place, mixed with its concentrate on innovation and consumer personalization, positions Sew Repair favorably in a aggressive retail panorama.

SFIX Inventory’s Valuation Engaging

From a valuation perspective, the inventory presents a gorgeous alternative, buying and selling at a reduction relative to historic and business benchmarks. With a ahead 12-month price-to-sales ratio of 0.29, beneath the five-year median of 0.50 and the business’s common of 1.14, the inventory provides compelling worth for traders searching for publicity to the sector. The inventory at the moment has a Value Score of A, additional validating its attraction.

Picture Supply: Zacks Funding Analysis

Estimate Revisions Favor Sew Repair Inventory

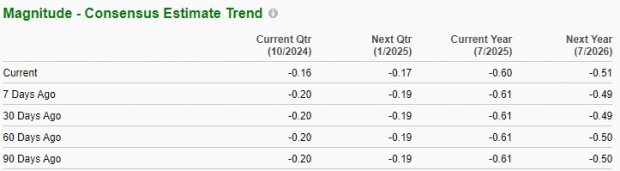

The Zacks Consensus Estimate for adjusted loss has been revised downward, reflecting the constructive sentiment round Sew Repair. Over the previous seven days, analysts have decreased their adjusted loss estimates by 4 cents to 16 cents per share for the present quarter and by 2 cents to 17 cents for the subsequent quarter. These estimates point out year-over-year development of 27.3% and 19.1%, respectively.

Picture Supply: Zacks Funding Analysis

SFIX’s Lowering Energetic Consumer Base: A Main Hurdle

Sew Repair faces a major problem with its declining lively consumer base, which has been a main contributor to the corporate’s income lower over the previous eight quarters. Within the third quarter of fiscal 2024, the variety of lively purchasers fell to 2,633,000, marking a considerable 20% year-over-year decline.

Because of this, the corporate skilled a income drop of 15.8% within the fiscal third quarter. This ongoing decline in gross sales factors to persistent difficulties in consumer retention and acquisition, highlighting deeper points associated to product attraction or heightened competitors out there. Shares of the corporate have misplaced 28.6% previously three months towards the Zacks Retail – Apparel and Shoes business’s 3.7% development.

Wrapping Up

Traders might contemplate SFIX resulting from its strategic concentrate on enhancing consumer experiences and sustaining a strong monetary basis, together with a debt-free stability sheet. The corporate has demonstrated the potential for sustained profitability by means of personalised procuring experiences and progressive use of AI, which has improved operational effectivity.

Regardless of challenges comparable to a declining lively consumer base, the corporate’s dedication to innovation and development positions it effectively within the evolving retail panorama. Sew Repair at the moment carries a Zacks Rank #3 (Maintain).

Shares to Contemplate

Some better-ranked shares are Nordstrom Inc. JWN, Abercrombie & Fitch Co. ANF and Crocs, Inc. CROX.

Nordstrom is a number one trend specialty retailer in the USA. The corporate provides an intensive collection of each branded and private-label merchandise. It at the moment sports activities a Zacks Rank #1 (Sturdy Purchase). You may see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Nordstrom’s fiscal 2024 gross sales signifies development of 0.6% from the fiscal 2023 determine. JWN has a unfavorable trailing four-quarter common earnings shock of 17.8%.

Abercrombie is a specialty retailer of premium, high-quality informal attire. It sports activities a Zacks Rank of 1 at current. ANF delivered a 16.8% earnings shock within the final reported quarter.

The consensus estimate for Abercrombie’s fiscal 2025 earnings and gross sales signifies development of 63.4% and 13.1%, respectively, from the fiscal 2024 reported ranges. ANF has a trailing four-quarter common earnings shock of 28%.

Crocs provides all kinds of footwear merchandise, together with sandals, wedges, flips and slides that cater to individuals of all ages. It at the moment carries a Zacks Rank of two (Purchase).

The Zacks Consensus Estimate for Crocs’ 2024 earnings and gross sales signifies development of 6.8% and 4%, respectively, from the 2023 reported figures. CROX has a trailing four-quarter common earnings shock of 14.9%.

Zacks Names #1 Semiconductor Inventory

It is only one/9,000th the scale of NVIDIA which skyrocketed greater than +800% since we beneficial it. NVIDIA continues to be robust, however our new prime chip inventory has far more room to increase.

With robust earnings development and an increasing buyer base, it is positioned to feed the rampant demand for Synthetic Intelligence, Machine Studying, and Web of Issues. World semiconductor manufacturing is projected to blow up from $452 billion in 2021 to $803 billion by 2028.

See This Stock Now for Free >>

Abercrombie & Fitch Company (ANF) : Free Stock Analysis Report

Nordstrom, Inc. (JWN) : Free Stock Analysis Report

Crocs, Inc. (CROX) : Free Stock Analysis Report

Stitch Fix, Inc. (SFIX) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.

{kind=link}