- US data revive recession fears, add to pivot view

- Yen recovers post-BoJ losses, stays in uptrend

- Euro awaits ECB minutes and Lagarde’s speech

- S&P 500 comes under pressure after testing key downtrend line

Weak data add credence to Fed pivot hypothesis

The US dollar finished Wednesday mixed against the other major currencies and continued in a similar fashion today. It is trading higher against the risk-linked and , while it is down against the yen. Against the rest, the greenback is trading in narrow ranges.

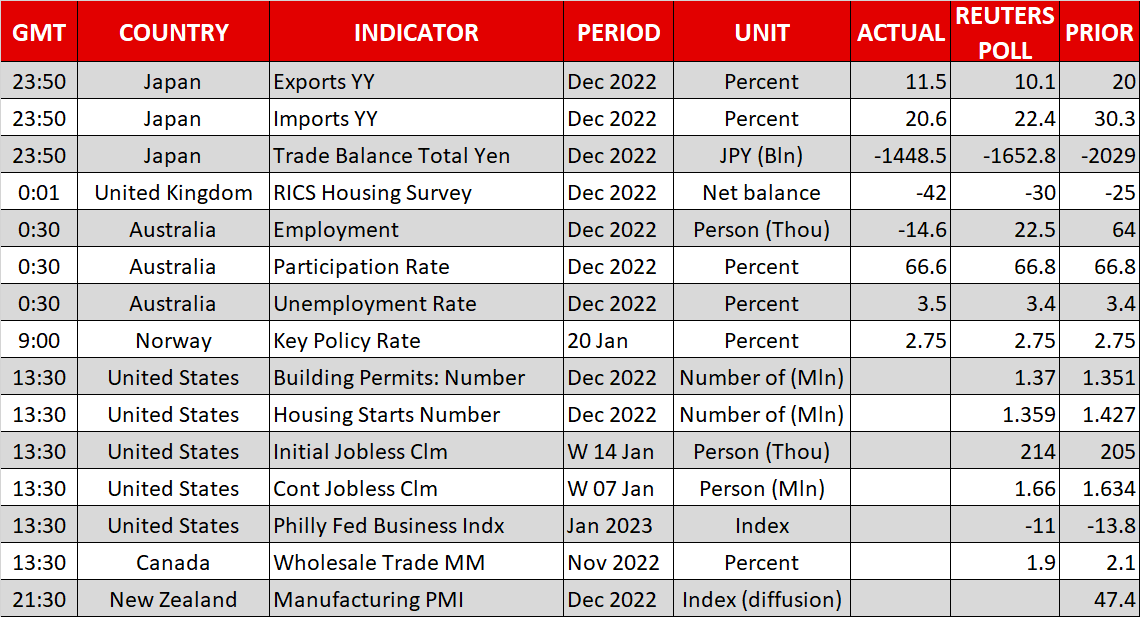

Yesterday, it was all about the US data. Both headline and core retail sales for December fell by more than expected, with the November figures being revised lower. Industrial and manufacturing production numbers also disappointed, while producer prices slowed by more than expected in yearly terms, with the monthly headline rate falling to -0.5% from 0.2%, missing the -0.1% forecast.

All these numbers may have refueled fears about a recession in the US, with the PPI data adding to the narrative that inflation is likely to continue cooling in the coming months. As such, investors may have remained convinced that the effect of the previously delivered rate increases is not fully felt by the economy yet, and that the Fed may be forced to cut interest rates at some point later this year.

Indeed, according to Fed funds futures, market participants have lowered their implied terminal rate to around 4.85%, even as St Louis Fed President Bullard and Cleveland Fed President Mester reiterated the view that interest rates may need to rise beyond 5%. More importantly, investors are now pricing in slightly more than 50bps worth of rate cuts by the end of the year.

The reason why the dollar did not fall after the data may have been safe-haven flows. Someone could argue that the hawkish remarks by Fed policymakers may have also helped, but the market pricing suggests that investors are still in strong disagreement with the Fed’s assessment. That said, even if the dollar continues to act as a safe haven for a while longer, it is unlikely to reclaim the status of the “ultimate safe haven”. With Treasury yields declining, investors may prefer gold and the Japanese yen and thus, the US dollar may resume its latest downtrend soon.

Yen wears safe-haven suit, traders still expect more from BoJ

The yen is the main gainer today, reversing all the losses it recorded after the BoJ’s decision to stick to its ultra-loose monetary policy. This likely adds to the notion that investors are sticking to the view that the BoJ is starting its own tightening crusade at a time when the Fed is headed for the exit.

Yes, the yen may have attracted sizable safe-haven flows after the US data revived recession fears, but if market participants were convinced that the BoJ will not take another step towards a tighter policy, they may have not bought the Japanese currency. After all, when other major central banks were tightening aggressively and the BoJ was holding back, they were actually selling the yen, even during periods of anxiety.

After yesterday’s decision, investors may have just pushed their expectations about the BoJ’s next move to the April meeting, after Governor Kuroda steps down and after the “shunto” spring wage negotiations. Therefore, with the Fed expected to cut later this year and the BoJ seen removing more accommodation, dollar/yen may be destined to continue drifting south.

Euro slides below $1.0800, awaits ECB minutes and Lagarde’s speech

Following reports that ECB officials are considering slowing their rate increments at the March gathering, the euro has been trading numb, with euro/dollar closing below 1.0800 yesterday. However, money markets are still pricing in a 50bps hike in February and almost another one of the same size in March, which means that traders have not drastically altered their view after the report.

Today, we get the minutes from the latest ECB meeting, as well as a speech by President Lagarde at the World Economic Forum in Davos. Should the minutes have a hawkish tone and Lagarde reiterates the view for more double hikes, euro/dollar could rebound and resume its prevailing uptrend.

Wall Street feels the heat of disappointing data

Wall Street suffered yesterday after the weak US data pushed back on the soft-landing narrative, with all three of its main indices losing more than 1% each. The S&P 500 and the Dow Jones recorded their biggest daily slides in more than a month, with the former coming under pressure after testing the key downtrend line drawn from the high of January 4, 2022.

It seems that bad economic data is slowly becoming bad for stocks, as deep economic wounds are anything but positive for companies’ earnings. Actually, some economic weakness is expected to be reflected in the current Q4 earnings season, with year-over-year earnings from S&P 500 expected to have declined 2.2%. However, estimates have declined notably heading into the season and thus, anything pointing to a slightly better picture could allow a relief bounce.

{kind=link}