- Wall Street headed for weekly losses as hawkish Fed talk pushes up yields

- But dollar mixed as investors await more clues on inflation

- Yen gains on BoJ nomination reports, oil jumps as Russia cuts output

Recession fears intensify as yield inversion deepens

Equity markets look set to end the week on a sour note as investors finally seem to be heeding the message from the Fed that the rate-hike cycle has some way to go following a series of hawkish commentary this week from Fed officials. Fed Chair Powell’s balanced tone on the inflation outlook has been overshadowed by sterner language from his colleagues about the risks from easing up on rate increases too early, with the Richmond Fed’s Barkin being the latest to voice his concerns on Thursday.

Powell has been surprisingly relaxed about financial conditions loosening substantially in recent weeks but that may be just a guise and the Fed is planning to quietly raise rates several more times this year. Initially, markets fell for this somewhat less hawkish stance but sentiment started to shift after last Friday’s super-hot jobs report.

There is no doubt that the NFP shock was a game changer as Treasury yields have been rallying since. But the most worrisome part about the US bond market right now is that the surge in yields has mostly been concentrated at the shorter end of the curve.

The yield curve inversion between two- and 10-year yields just got deeper, inverting the most since the early 1980s yesterday.

Stocks turn negative for the week

Whilst this does not necessarily mean that a recession is a foregone conclusion in America and there are still hopes that a soft landing will be the eventual outcome, it does nevertheless underline the stress in the markets about the Fed lifting rates too high and this is a problem for Wall Street.

Despite some earnings beats and outperformers such as Tesla (NASDAQ:), both the S&P 500 and Nasdaq are on track to end the week lower. But with the earnings season starting to slowly wind down, investors’ main focus now is on the January CPI numbers due next Tuesday as they could be the only thing to halt the rise in yields in the short term if they are soft again. Ahead of that, the University of Michigan’s preliminary consumer sentiment readings will be watched later today for more evidence that consumers’ inflation expectations are coming down.

Dollar lacks direction, yen likes new BoJ governor nominee

The US dollar continues to drift somewhat lower on Friday as it struggles to build on the post-Fed bounce from last week. Although there’s been a significant repricing in money markets over this period and the market-implied terminal rate for the Fed is back above 5%, this ‘realignment’ comes at a time when other central banks remain just as, if not, more hawkish. Hence, why any upside for the greenback has been limited lately and will likely continue to be limited for some time.

As long as the inflation data is pointing to faster disinflation in the United States than elsewhere, the dollar doesn’t stand much of a chance for a meaningful rebound.

But for today, the main drag on the is the yen. The Japanese currency is up across the board after jumping on reports that the Bank of Japan’s dovish deputy chief Masayoshi Amamiya has turned down the offer to replace outgoing Governor Haruhiko Kuroda.

Former board member Kazuo Ueda is being billed as the likely candidate that the Japanese government will nominate next week to head the BoJ. Ueda has been known to oppose rate hikes in the past and in surprise remarks today he backed the current easy policy stance of the BoJ, so he may not be that much less dovish than Amamiya. Nonetheless, there seems to be some relief among yen bulls and the dollar briefly slipped below 130 yen earlier in the session before paring its losses.

China recovery doubts hurt , and oil boosted by Russian cuts

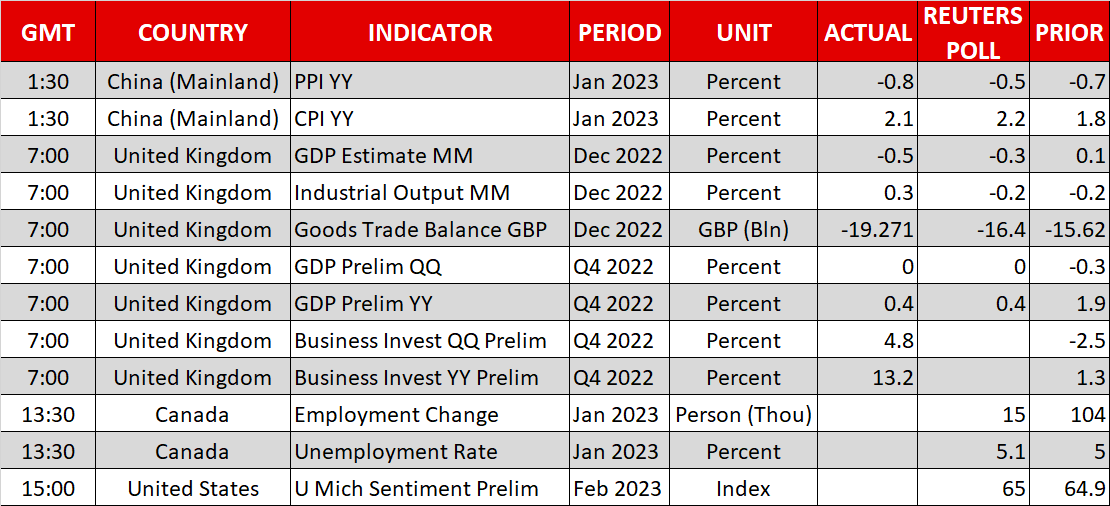

The Australian dollar is trading flat versus the greenback today as stronger inflation projections by the RBA in its quarterly Monetary Policy Statement were offset by weak consumer and producer price data out of China. Both CPI and PPI came in below expectations in January, casting doubt about the strength of demand recovery in China following the reopening.

The Canadian dollar, meanwhile, was slightly firmer ahead of Canadian employment figures due later in the day. The jobs data will probably not have much impact on the domestic policy outlook, but higher oil prices are supporting the loonie today. Oil futures surged by more than 2% after Russia unexpectedly announced a cut in crude production of up to 500,000 barrels a day.

{kind=link}